Can American Express do what Visa and Mastercard cannot? (with agentic commerce)

Understanding the advantages of a closed-loop network for new payment paradigms

Welcome to Payments Culture!

This newsletter explores how money moves, around the world — and why it matters.

I recently spoke with Margaret Ryan, SVP and Head of Product at Amex Digital Labs to learn more about American Express’ recent product announcement on the topic of agentic commerce. Our conversation started with the big picture:

We see agentic commerce as the next era of digital commerce. Things are changing. There’s a fundamental shift happening in how customers are searching for things, how they’re discovering products, and booking travel. And ultimately how that payment is happening. We want to make sure that we are, where our customers are.

What follows are my reflections on the conversation, a look at how Amex is approaching agentic commerce, and why their approach differs.

If you work in payments you’ll be used to reading about agentic commerce. It’s impossible to avoid. This year has seen a slew of announcements on the topic. Often, it’s hard to understand which announcements are actually relevant, and which are companies shipping news to stay in line with the competition. It’s corporate FOMO.

Everyone wants to be at the front of the pack, but it’s confusing. Those who don’t get front and centre in the agentic commerce discussion risk getting left behind.

Agentic commerce payment volumes are low, but we are caught in a frenzy of agentic commerce protocol soup.

How many fintech professionals really know their MCP, from their UCP, and their AP2? Making it more complicated is the fact that A2A is now a double synonym. For a long-time A2A was account-to-account payments, yet now A2A is also Agent2Agent, another protocol, one which allows AI agents to exchange information with each other. Visa and Mastercard have launched their own protocols too. Visa’s TAP helps merchants verify and transact with agents, and Mastercard’s Agent Pay does a similar job on their network. Coinbase started x402 as an open payments protocol, but today, it sits within the Linux Foundation with a vendor-neutral governance structure.

From x402’s homepage:

Payments on the internet are fundamentally flawed. Filling out a form is a human behavior that doesn't match the programmatic nature of the internet. It's time for an open, internet-native form of payments. Payments that are amazing for humans and AI agents.

x402 is one of the protocols that people are most excited about. Yet as of early May its annualised run rate is around $300m, an amount which flows through Visa’s network in less than ten minutes.1

Every new protocol, or evolution of a protocol, promises to be a game changer. But for merchants, platforms, banks, fintechs, and others, the challenge is moving from a world in which payment protocols have remained the same for decades — I’m thinking of ISO 8583 — to one in which new protocols are appearing every month. Of course, it’s not all payments specific. The term-commerce often does a lot of lifting as verification and trust are key parts of agentic commerce.

With all this in mind, American Express’ recent agentic commerce announcement allowed me to breathe a sigh of relief. They were not launching a new protocol.

Understanding Amex’s offering

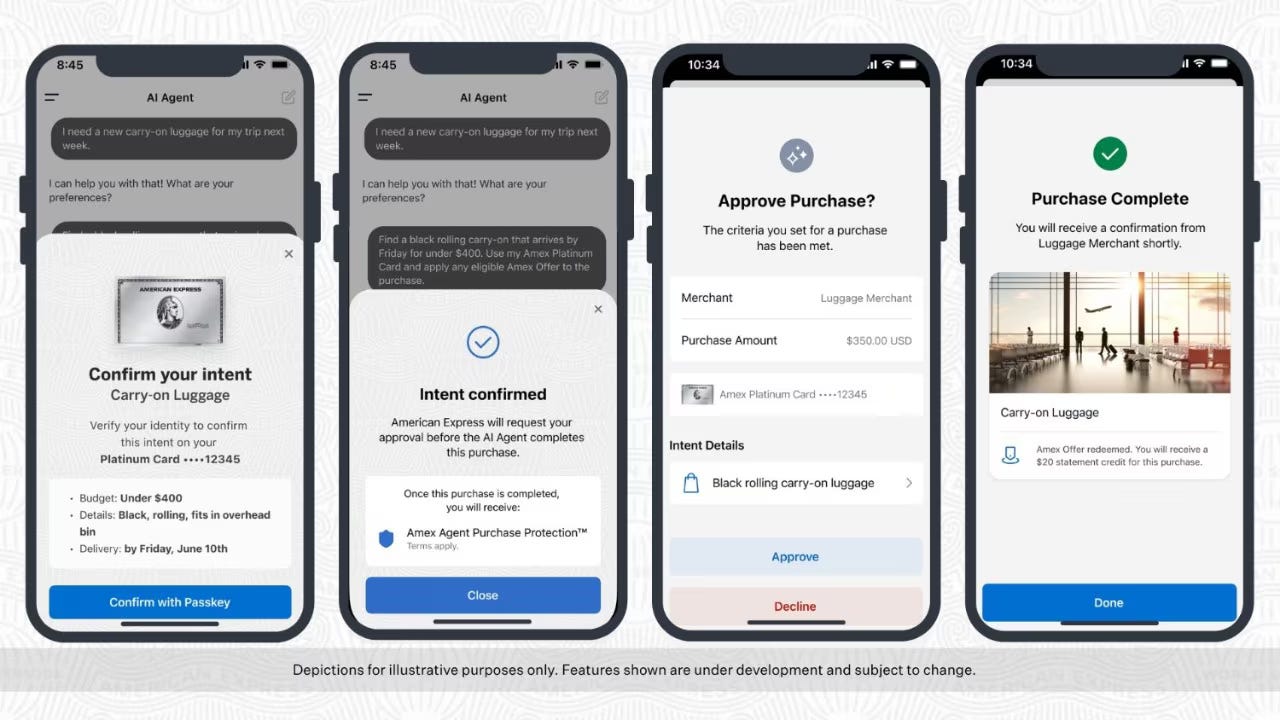

Recently American Express (Amex) launched the Agentic Commerce Experiences (ACE)™ Developer Kit and what they cite as an industry-first protection for Registered Agent Purchases.

The Amex Agentic Commerce Experiences (ACE)™ Developer Kit is a framework that provides technical specifications to bring American Express-issued Cards and Membership value into AI-powered interactions with trust and control. Designed for flexibility and interoperability with existing and emerging protocols, the ACE Developer Kit will enable intent-driven transactions with end-to-end visibility across the commerce lifecycle through Amex’s closed-loop network.

I’ve highlighted the sentence where Amex makes it explicitly clear that Amex is working with existing protocols, which is a change in approach compared to many payments companies of Amex’s size.2 Margaret told me that “ACE is built to be interoperable with all of the existing as well as emerging protocols”, adding that “standardization is important because that's the only way to really get this to scale.”

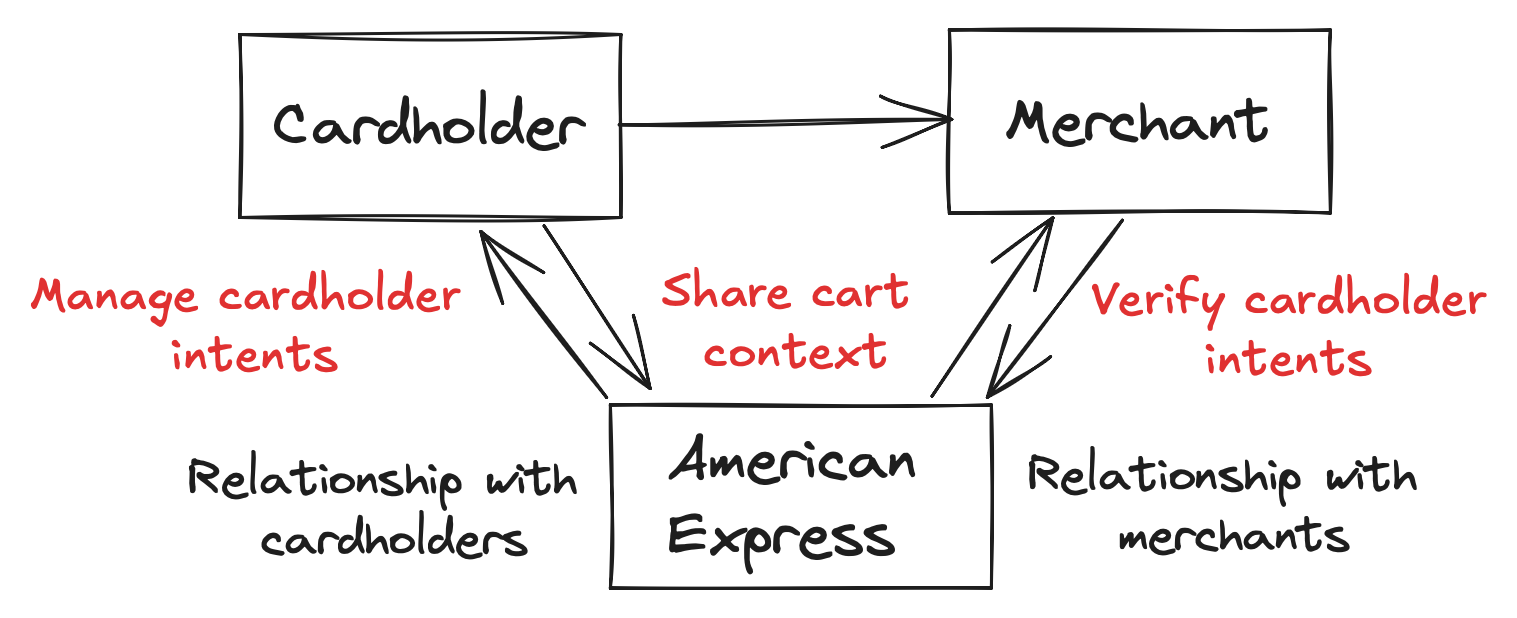

Interoperability is a path many payments companies are taking. For example, Amex endorses the Universal Commerce Protocol (UCP) alongside companies such as Stripe, Visa, Mastercard, Adyen and Shopify. However, unlike Visa and Mastercard, Amex has not launched their own protocol. Partly, this is reflective of differences in business model. Visa and Mastercard sit as a coordination layer between issuers, acquirers, and other third parties, whereas Amex’s closed-loop model means their approach differs as they have direct relationships with both merchants and cardholders.

The move from single payments to payment intents is one of the biggest changes to have happened in payments in the past few decades. Wherever they sit in the value chain, payments companies need to deal with this change and understand how they can best support this paradigm shift. However, the change will be gradual and at first incremental. It may take some years before even 10% of payment transaction volumes are intent driven, yet Amex is looking to get ahead and support their merchants and cardholders as interest in the technology grows.

It’s worth outlining some of the key differences in how the single transaction and intent models impact the user payment journey.

Single transactions:

Each transaction requires authorisation at the time of purchase. The authorisation confirms that funds are available, and that the cardholder consents to the transaction. Various parties check for potential fraud triggers.

The cardholder uses face ID to pay with Apple Pay, enters a code for a one click check out, or taps their card for contactless payment.

If something goes wrong — such as the merchant charging for an incorrect amount, or the cardholder not receiving the goods they paid for — then the cardholder can initiate a dispute3 for that specific transaction.

Payment intents:

A user defines the product they’re looking to buy alongside constraints such as price ceiling, merchant type, and the time frame for which the intent should be valid. That's the first stage of authorisation. The second stage happens against those constraints, without the cardholder needing to get pulled back into the authorisation flow.

The cardholder is involved at the outset but not for every transaction. It’s possible to revoke, or in some cases even adjust intents that have already been established.

If something goes wrong then the intent has to be considered. Did the agent act within the cardholder’s parameters? Existing dispute rights remain but agentic commerce introduces the new concept of one intent leading to potentially many transactions.

Agents and the dispute challenge

The dispute challenge in agentic commerce is an interesting one.

In theory agents should follow customer intents as described, yet as with any system, especially emerging autonomous systems, there’s always the possibility for error. Amex’s news release captures how they are looking to assuage the concerns customers may have when paying via an AI agent:

In the future, if a Card Member authorizes an AI agent to make a purchase and that agent sends American Express the customer’s authenticated purchase intent, American Express will protect eligible customers from charges related to AI agent error.

A couple of points to note here. The purchase protection is dependent on the agent sending Amex the authenticated purchase intent, which as per the earlier diagram, is authenticated via a passkey. Amex, as both a card issuer and an acquirer,4 has direct sight on both sides of a transaction, and while standard disputes can still be initiated, the added Amex Agent Purchase Protection provides a greater level of mitigation.

This scenario of an agent purchasing a product incorrectly was described by Margaret as follows:

The customer may ask their agent to buy a blue shirt, but the agent goes and buys a non-refundable black shirt. The merchant has done nothing wrong. They fulfilled based on the request they received. The customer has done nothing wrong, either. But the customer is now stuck with this shirt that they can’t return… With the Amex Agent Purchase Protection, we are backing our customers.

Essentially this is Amex saying to consumers: you may be concerned about setting up an intent, but if something were to go wrong we’ve got you covered.

On the merchant side, cart context — outlined in red on the above diagram — plays an important role in making agentic payments work for all parties involved. Amex is able to compare the agent’s shopping cart with the cardholder intent. The comparison can happen at the moment of authorisation. Any mismatches can be flagged before transaction completion or after the fact to aid any dispute resolution.

What can Amex offer which Visa and Mastercard cannot?

Cart context is a great example of where Amex’s closed-loop network offers a level of data sharing that is much harder for open-network players to build. For Visa and Mastercard to have the same functionality, card issuers and card acquirers would need to capture this data and provide it back to the card schemes. Not impossible but much harder in an open-network model. Amex is able to set a clear standard for its network and is working with large merchants, platforms and payment providers such as OpenAI, Stripe, Adyen, Hilton and Expedia.

For cardholders, managing intents is a new challenge for issuers to reckon with. Cardholders will want to see and track what intents are open, at any one time. As agentic payments grow in scale and scope, the ability for cardholders to see key information in one place, and track their open intents will prove to be powerful:

Within the Amex mobile app, the customer will be able to see where their card is linked to their agent accounts. They’ll be able to see intents that they have previously approved. They’ll also be able to cancel them and adjust them.

For other card issuers, the ability for cardholders to view intents will need to be built as a new feature in-app and online. Some issuers will do this better than others. Some will make open intents easy to manage and visible at a glance, and other will struggle to get this right. If anything, it may become an important factor in analysing the best bank or issuer to work with for agent-linked payments.

Amex’s solution is for the US market initially with others to follow at a later stage. Globally more merchants accept Visa and Mastercard, the two largest American card schemes, than Amex. Outside of the US, Amex often has higher fees than Visa and Mastercard, with the UK and EU being clear examples of this. In Europe, there are additional challenges to contend with for agentic payments, such as the requirements around Secure Customer Authentication (SCA). Passkeys go some way towards meeting these requirements, but the question of whether one SCA-compliant authentication at the intent stage covers all downstream agent transactions is an open question.

For me, the question remaining is whether consumers really want agentic commerce. The proof will be in the data and usage in the coming years. But what I genuinely do like about the Amex solution is allowing cardholders to see their intent info in one place. Sometimes payment solutions get ahead of themselves — the tech may be exciting, but getting the consumer experience right isn't always easy. Here, the closed-loop network model has allowed Amex to deliver on that. Visa and Mastercard compete in slightly different ways, and helping issuers manage intents efficiently for their cardholders will become a key deliverable across both networks.

Next time, I'll take a detailed look at the consumer demand for agentic commerce and whether the hype is deserved.

Thanks for reading Payments Culture. I appreciate it!

Please consider sharing this newsletter with a friend or colleague if you enjoyed reading this edition. If you are not yet a subscriber please sign up below for a free or paid subscription.

Note that views expressed on this Substack are my own and do not represent any other organisation. Also nothing I say should be taken as investment advice.

You can contact me on LinkedIn, Twitter (X), via email, and with the below button.

Writing on May 11th 2026, x402’s own data shows a transaction value of around $25m over the past 30 days, which annualises to a circa $300m run rate. Visa processes more than $16 trillion per year.

Amex’s market cap is more than $200bn, significant although much smaller than Visa at $600bn.

Note that in the world of Amex the term dispute tends to be used instead of chargeback. From the cardholder perspective the impact and process is largely the same. However, one big difference in the Amex model is the number of parties involved in dispute resolution. Amex is usually the issuing bank as well as the payment processor. For Visa and Mastercard there are more parties involved: as the card schemes, they manage the rules for chargebacks; involved are the acquirer who provides evidence to defend chargebacks on behalf of the merchant; and the issuer helps the cardholder raise a dispute when necessary.

In most markets Amex is a card issuer and acquirer. But there are some markets in which Amex allows local banks to issue cards under its brand. In such cases, Amex may maintain direct issuing alongside the bank partnership approach, or it may provision all Amex badged issuing activities to the local partner(s).