Do consumers really want agentic commerce?

Consumer adoption hasn't matched the headlines... yet

This week’s post is about agentic commerce and consumer payment habits.

It’s worth making clear at the outset that this isn’t an anti-agentic payments post. There’s enough substance in recent developments to say that payments and AI are clearly coming together, yet it’s worth taking a step back and looking at the gap between hype and demand. Over the past year an assumed inevitability has built up around agentic commerce, which the data doesn’t quite support. In the short term, the version of agentic commerce that will succeed is likely to augment, rather than recreate, the shopping experience. I explore this and more in the below essay.

Any comments or feedback are welcome. Feel free to leave a comment at the bottom of this post, or you can reach me directly via LinkedIn, Twitter (X), or email.

OpenAI’s thesis was that AI could collapse that entire [buying] process into a conversation. Ask ChatGPT what running shoes to buy for a half marathon, and instead of a list of links, you get a recommendation, a reason, a price, and a button. One tap, done.

- Adrian Gmelch writing on the Lengow blog

Last month Google held their annual developer event Google I/O 2026. Similarly to Apple’s WWDC event, Google I/O has in many ways gone beyond a developer conference and now serves as a general forum to announce product updates. The extent of the new developments were such that Google published a blog titled 100 things we announced at I/O 2026.

It’s hard to keep track of everything that got announced at the event. Especially as Google has such a variety of product names, whereas other companies like Anthropic put everything within the Claude brand. Reflecting this, Ben Thompson wrote in Stratechery:

There is a lot of AI spaghetti getting thrown against the wall in terms of products; we’ll see how much of it sticks.

Thompson's critique is something which is, ironically, also a strength.

He theorises that Google’s lack of focus is precisely why it endures. This is true. When using the internet it’s hard to avoid using Google’s ecosystem in some way shape or form. Google’s surface area stretches from docs to gmail to search to YouTube to Chrome and beyond. With Google permeating AI across its solutions, users often aren't choosing to use Google's AI tools — they are persistent and integrated as part of the user experience as standard.

From a payments perspective there were a few points of note, all under the heading of Universal Cart.

28. We’re introducing Universal Cart: a truly intelligent shopping cart and your new hub for shopping on Google. You’ll be able to add things to your cart while you’re browsing Search, chatting with Gemini, watching YouTube or even reading your Gmail. The moment you add a product, your cart goes to work for you in the background. It finds deals and price drops, gives you insights on price history and alerts you when something comes back in stock. The Universal Cart runs on our Gemini models, so your cart gets smarter as the models improve.

29. It also uses intelligent reasoning to anticipate your needs and help solve problems before they arise. It’ll proactively flag any product incompatibilities and suggest alternatives. And since the cart was built on Google Wallet, it understands your payment method perks, loyalty information and merchant offers so it can intelligently help you choose between payment methods.

30. Universal Commerce Protocol (UCP) makes checkout from your cart super smooth. For many of your favorite brands, you can check out right on Google in just a few taps with Google Pay, or transfer items straight to the retailer’s site and buy there.

I mentioned in an earlier post that agentic commerce is beset by a protocol soup. UCP is one clear example of an emerging protocol in the agentic payments realm. Others such as A2A and AP2 have also emerged in the past year and competition at the protocol level can be confusing.

Yet, Google’s reach gives it a unique position. It seems likely that many of us will encounter Universal Cart and UCP in the coming months and years (dependent on if and when it launches in your market, as much of this is US only for now). Agentic commerce is leading to a change in how companies interact in terms of the end-to-end product discovery and transaction flow. In some cases, companies will compete differently to today, and there will be a battle for who owns various elements of the payment stack. This specific topic of the agentic commerce layer cake and payments stack is worth further investigation in more depth in a future post.

Do consumers actually want this?

For the rest of today’s post, the key aspect I want to explore, is that despite all the announcements and hype, there’s often limited discussion in terms of whether consumers actually want agentic commerce.

What is agentic commerce? (and other hype cycles)

If you work in fintech you may hear the term agentic commerce every week, or maybe even every day. But it hasn’t always been like this. It’s a term whose origins are relatively recent. ChatGPT launched in December 2022, and while fintech has worked with facets of AI — such as machine learning in areas including fraud prevention — for many years, the growing popularity of LLMs has led to new possibilities for agents to lead users from product discovery-to-purchase.

One of the first mentions of agentic commerce was in November 2024 in a blog by Scott Friend of Bain Capital Ventures titled The Dawn of the Agentic Commerce Era. In the post the author explores how intelligent shopping agents could shape the world.

An intelligent shopping agent will know everything there is to know about our individual and family needs, our tastes, our existing “inventory” and, importantly, our budget. Armed with this data, our agent will not just suggest alternatives but will, in fact, complete the entire shopping mission on our behalf.1

This new paradigm will unlock huge amounts of time and savings for consumers. But, will it be equally beneficial for merchants?

Reading this reminded me of earlier technology hype cycles. Do you remember the Internet of Things (IoT)? Even though we rarely hear the term these days, it’s still around and by some measures generating significant revenue. Statista Market Insights forecasts that IoT revenue in the US alone to be worth more than $400bn in 2026.

IoT revenue is mainly in industrial sectors, and emerging technology areas such as self-driving cars. The consumer segment hasn’t proven as popular as once expected.

Back in the 2010s there was a lot of fuss about IoT. It was touted as the next big thing. In the future, our fridges would automatically order our products for us when we run low (I actually saw a presentation on this very topic given by someone from a large credit card company). Considering they make everything from fridges to phones to vacuum cleaners, companies like Samsung were seemingly well placed to capitalise on the IoT trend. Funnily enough I did end up getting a robot vacuum cleaner which connects to the internet. It’s Chinese and not Korean. Although my fridge is still an analogue one. But I do have a Samsung TV.

IoT was a strange hype cycle. Gradually we did connect more of our devices. Largely due to the expectation, which developed in the past decade that everything should be managed directly from our phones, an expectation which wasn’t prevalent at the dawn of the IoT hype. So rather than ordering new products directly from our appliances, IoT instead primarily became a way for us to manage devices from our central personal hub — our smartphones. Additionally, early IoT hype was held back by a lack of horizontal integrations. In order for a fridge to be able to order milk it would need to connect to a supermarket delivery service and in most markets such integrations were lacking. Whether it be Samsung or someone else, no IoT provider owned hardware, software and product distribution.

Will agentic commerce follow the same path as IoT? At least on the consumer level, which is the focus of this post, then it’s likely that the hype will be ahead of the demand for some time. The scale and speed of consumer adoption is always hard to predict. We may all start paying with, and through, AI-based interfaces if it becomes unavoidable — especially if every major tech and payments company offers it as standard. But history teaches us that what seems inevitable doesn’t always turn out that way.

Two other examples come to mind.

Remember when Visa paid around $150,000 (the price of 49.5 ETH at the time) for CryptoPunk #7610? NFTs crashed and burned rather quickly. They did not have “an important role in the future of retail, social media, entertainment, and commerce” as Visa once predicted. And who can forget the Metaverse? Citibank estimated that the metaverse economy had a potential addressable market of $8-13 trillion with the prospect of reaching 5 billion users by 2030.2 Nowadays the term is rarely mentioned, or only mentioned in retrospective.

Looking back it seems obvious why these trends didn’t take off. Yet at their height, the hot money was flowing in to these developments and big corporations were spending big not to miss out on the next big thing. AI as a general trend does seem more robust. It’s already embedded into large chunks of the economy. But it’s useful to consider that what once seemed obvious and inevitable doesn’t always come to fruition. For agentic commerce, I estimate it will be something which consumers gradually get used to, and will take time, more time than many expect.

Note: An Edgar, Dunn & Company report from earlier this year mentions that they expect agentic commerce to reach 15-25% of e-commerce volume by 2030. Interestingly, in what’s potentially a sign that researchers have learned lessons from the overly optimistic projections of the Metaverse et al the report explicitly mentions that their projection avoids “any inflated” total addressable market.

Chasing the hype but what’s the reality?

Like most tech forward industries, the fintech world is great at concocting terminology. But soon the latest terminology can only be explained with reference to other terminology, yet often no one really knows what it all means. You can get to a stage where asking too many questions seems awkward and asking ChatGPT doesn’t help. (Unless carefully questioned LLMs can regurgitate terminology inside only a shadow cloak of understanding.) It’s easy to say that the latest tech will change the world but being able to say precisely how and why is much harder.

Enter agentic commerce. The description from Scott Friend of Bain Capital Ventures noted above should have been enough. It clearly explained what agentic commerce is. Agents will know everything about our needs, tastes, inventory and budget. They’ll complete our shopping for us. The key to agentic commerce, as originally defined, is the end-to-end flow from knowledge about shopping habits to the transacting and shopping itself.

What’s happened in the past year is that in an effort to ride the AI wave, many companies have positioned their offerings as agentic commerce, even when they were, by the original definition of the term, not agentic commerce. This dynamic is common. When a phase becomes fashionable, vendors race to attach themselves to it for marketing reasons, and what was once a useful concept turns into a label that means everything and nothing. Everything which brings together AI and payments in some way now gets referred to as agentic commerce.

What’s often missed is that the success of agentic commerce as envisaged by Scott Friend and others requires consumer buy in. No matter how good the tech may be, if consumers are not sold on agents completing their shopping for them then it won’t happen. The gap between what users want today and where the industry wants to take them is substantial.

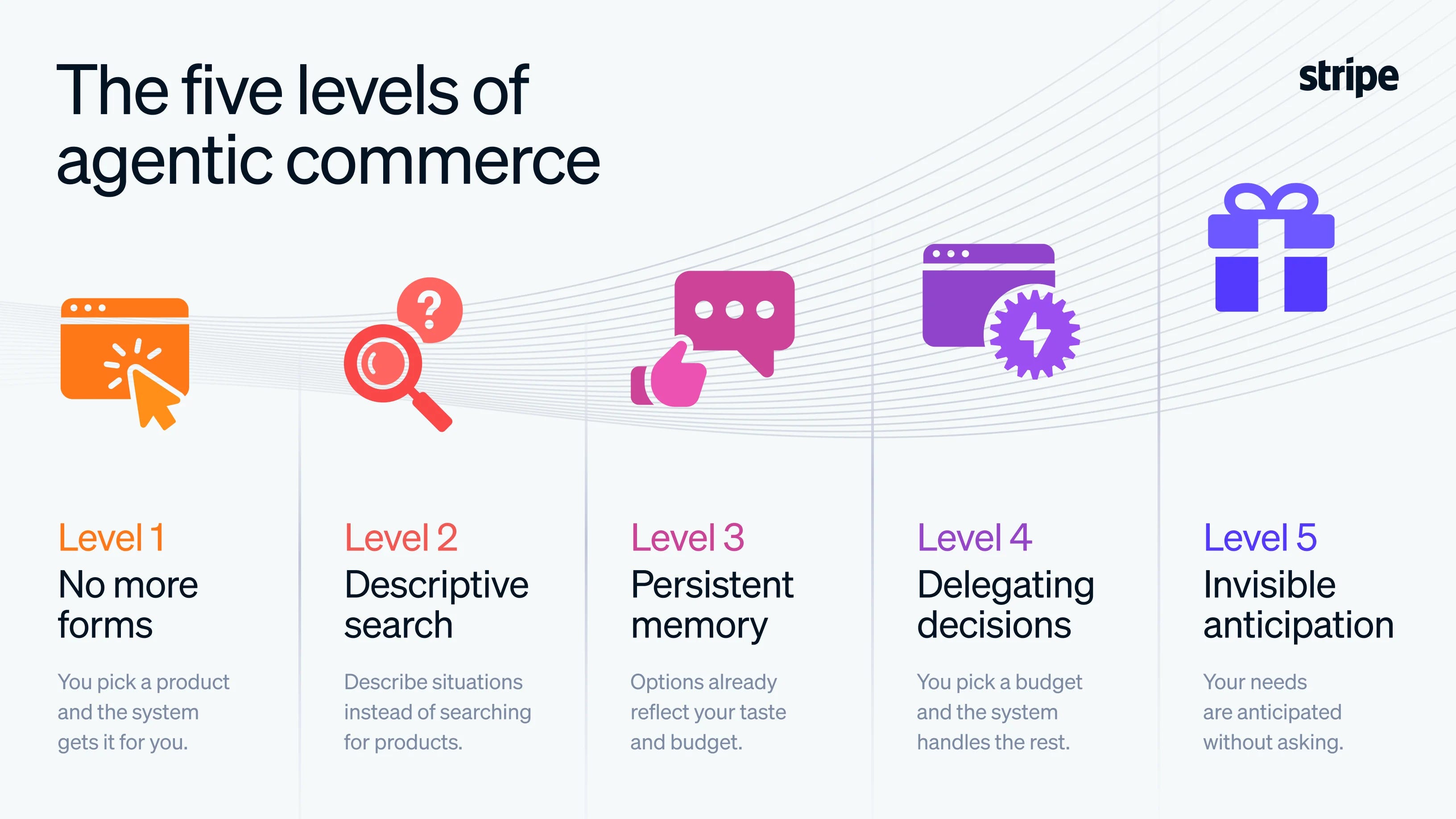

Stripe’s 2025 annual letter, published in February 2026, provides a useful break down of what they refer to as levels of agentic commerce. Essentially degrees of autonomy in dealing with AI agents. At each level the extent of human input diminishes.

Level 1: Eliminating web forms

You research and decide what to buy. But filling out web forms is no one’s favorite way to spend a few minutes. It would be handy if you could simply send the URL to your agent and have it fill out your payment and shipping details, coming back to you with the confirmation.

The system isn’t making any decisions; it’s just typing and clicking “buy” on your behalf.

Level 2: Descriptive search

You stop searching for products or specific attributes and start describing situations.

I need back-to-school supplies for a third grader in Chicago, including clothes (nothing too itchy or tight!), pencils, notebooks, and a lunch box. My son likes K-Pop Demon Hunters and tennis. School starts in late August.

The system reasons across weather, materials, sizes, durability, taste, reviews, and delivery timelines. Specialized and long-tail products become easier to find. Annoyingly blunt keyword search is no longer a thing.

Level 3: Persistence

You stop reintroducing yourself.

Find me options for back-to-school clothes for Bobby.

The system already knows your preferences and remembers any requirements, inferred from your previous conversations and purchases. You’re still deciding what to buy, but you are choosing from a set of options that already reflects your taste and budget.

Level 4: Delegation

You stop choosing altogether.

Get the back-to-school shopping done. Keep it under $400.

The system handles the search, the evaluation process, and the purchases on your behalf. You trust it will weigh trade-offs as you would and choose things your son will like. All you do is determine the budget. (This is what most people mean today when they talk about agentic commerce.)

Level 5: Anticipation

There is no prompt.

The system already knows the school calendar, your son’s preferences, and your typical budget. All you do is receive a notification: here’s the back-to-school list of everything that’s been purchased. This is the most futuristic vision, where the things you need show up right before you need them, without you having to ask.

Agentic commerce as originally defined would be at levels 4/5 of Stripe’s categorisation. In the same letter Stripe states that we are currently “hovering on the edges” of levels 1 and 2. But are we even at levels 1 and 2 in terms of broad consumer demand?

In April of this year, McKinsey surveyed over 3,000 consumers in the US, and the output can be seen in the report Shopping in the age of AI: Redefining stores for a new era. It found that AI demand is most common in the early stages of the shopping journey, and that “by 2030, the US B2C retail market alone could see up to $1 trillion in revenue from agentic commerce”. In reality, this revenue figure will depend on how revenue from agentic commerce is defined. An earlier McKinsey report referred to “orchestrated revenue” from agentic commerce having a potential market of up to $1 trillion, which allows a lot of room for manoeuvre.

Other data shows a mixed picture.

Research by Clutch found that while 65% of consumers have used AI to research products before making a purchase, only 4% of those surveyed would be happy to let AI complete a purchase on their behalf. Data by Bain shows that “30% to 45% of US consumers currently use Generative AI for product research and comparison”, yet at the same time 50% of customers are not comfortable allowing AI to make purchases on their behalf. As the full survey data was not published it’s hard to draw conclusions either way on whether only 50% were comfortable or if there’s further nuance here.

Preferences reveal themselves more in actions than in words. If consumer surveys are unclear on whether consumers are ready to embrace agentic commerce, can real-world case studies help us better understand the demand?

The October frenzy

Possibly the most important announcement of the past year took place at the end of September 2025. Stripe and OpenAI unveiled Instant Checkout in ChatGPT. With this announcement I naively thought that’s it. For a brief moment it seemed as if agentic payments was solved. I was wrong and so were many others.

Further announcements took place in September and October including ones from Mastercard and PayPal, but the Instant Checkout one really stood out. This would be the first time that users could actually pay within ChatGPT directly. Companies such as Walmart signed up to Instant Checkout. Target soon followed.3 ChatGPT was by far the most popular AI app, with around 700m users at the time, which has risen to 900m today. This solution brought together some of the world’s largest retailers with the best-known AI app. Momentous.

The growth in interest in agentic commerce following the Instant Checkout announcement led to a rise in attention-side demand — when consumers became aware of agentic commerce. The news made waves throughout the media and was picked up both within the payments industry and by general news outlets. Momentum has continued way past the search trend peak. The adoption is another story.

Instant Checkout in ChatGPT made sense on paper. If users are using AI for discovery then it logically follows that checking out in app without redirection would be the most frictionless way to pay. In fact, payments have, for a long time worked on the basis that the less friction the better. Online payment methods have lived, or died, by minimising the number of clicks or taps at the checkout. Everything was in place for Instant Checkout to be a success.

A long-read in Modern Retail explained further how both buyers and sellers would benefit:

The feature allowed users to ask ChatGPT what they’re looking for and receive recommendations of relevant products from across the web. For merchants with Instant Checkout enabled, buyers would confirm shipping details and pay the merchants directly from the ChatGPT app. The retailers would handle fulfillment, returns and customer support themselves.

Despite the promise things didn’t work out. Walmart found, when given the choice of completing a purchase via ChatGPT or a redirection to their homepage to complete the purchase, users preferred the latter option by a factor of three.

Why didn’t Instant Checkout in ChatGPT win? Partly, as discussed earlier, but proven to be even more the case here, LLMs are great for research and discovery, but users prefer to go to an existing trusted source to complete a purchase. Consumer habits are hard to change.

OpenAI staff realized that ChatGPT users were researching products to buy but weren’t using it to help them make purchases.

Other issues soon became apparent.

Many retailers sat back and watched how Instant Checkout would evolve, not quite ready to give away the checkout experience to OpenAI. But there were also product level issues as within Instant Checkout users could only purchase one item at a time. There wasn’t the concept of a shopping basket, and for large retailers pulling in live SKU data for hundreds of items was a technical challenge, which didn’t warrant engineering resource until the demand was proven. The goal was to prove the demand at the consumer level and then the additional supply, meaning more merchants, would soon follow and sign up to Instant Checkout. This goal wasn’t realised.

After six months of live data, merchants and OpenAI were able to assess the situation this spring. The company announced changes to Instant Checkout in March, noting with some contrition that:

Our North star is providing the best experience for both consumers and merchants. The best consumer experiences are powered by deep partnership with merchants. To build these deep partnerships, we want to offer merchants options for how they convert consumers. We’ve found that the initial version of Instant Checkout did not offer the level of flexibility that we aspire to provide, so we’re allowing merchants to use their own checkout experiences while we focus our efforts on product discovery.4

Yet in early 2026 the AI coding wars were big news. Anthropic’s Claude Code was everywhere, and in Q2 OpenAI’s Codex product has gained ground. Some “consumer focused initiatives have been sidelined” — including Instant Checkout, which still exists but is much less of a focus. The company sees enterprise revenue as more dependable. Many consumers use ChatGPT without a paid subscription. The balance and attention has shifted from chat to agent-led applications.

Making agentic commerce work?

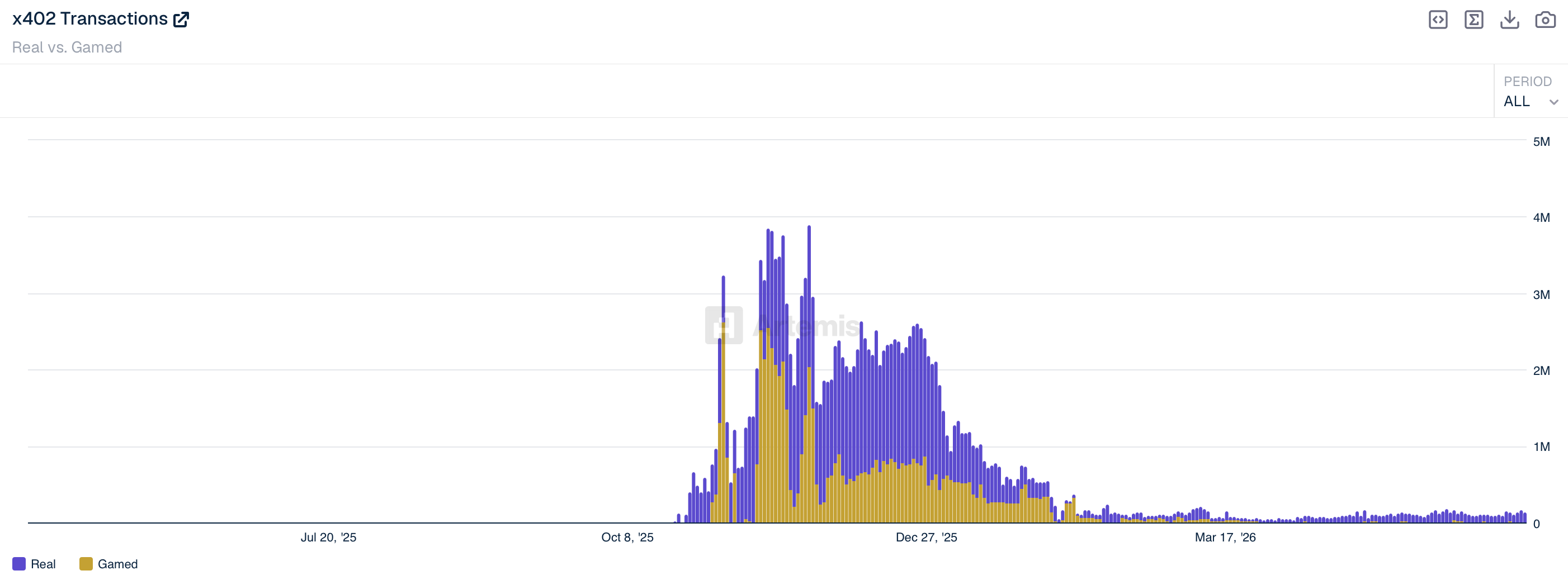

While the focus of this essay has been on agentic commerce from a consumer lens, much of the recent activity and announcements have shifted towards agent-to-agent payments. Stripe and Tempo launched the Machine Payments Protocol (MPP), and even in the past few days Mastercard announced Agent Pay for Machines (AP4M), which offers "a new class of payments" specifically for AI agents. So far the noise around machine-to-machine payments has been considerable, but there's little public indication of actual transaction volumes.

The one payments protocol for machine payments that does have public volumes available is x402, a protocol that was started by Coinbase that runs primarily on the Base blockchain. Data available on Artemis, an analytics firm, shows that x402 transactions grew rapidly in October 2025 and peaked in November before declining and tailing off in 2026.

Back to the consumer side, despite the challenges of OpenAI’s Instant Checkout, this isn’t to say that agentic checkout will never work. It can be useful in specific verticals, although booking a flight may not be one of them — despite being a use case that strangely keeps coming up. Booking flights is too high-value to delegate entirely to AI and the risk and cost of getting it wrong is too high (for me at least). Other areas still make sense, and it’s in the interest of some of the world’s biggest public and private companies to make it work.

In a future post: how to make agentic commerce work for consumers, with examples from Google, what’s worked in China, and my own thoughts on what’s needed to embed and augment existing shopping experiences.

Please consider sharing this newsletter with a friend or colleague if you enjoyed reading this edition. If you are not yet a subscriber please sign up below for a free or paid subscription.

Note that views expressed on this Substack are my own and do not represent any other organisation. Also nothing I say should be taken as investment advice.

My bold

More than half the world’s population!

An excellent overview of the timeline of various retail interest in Instant Checkout can be found on the Lengow blog

My italics

Great exploration of the friction layer in automated commerce, Matt. The massive gap here isn't just consumer psychology—it's how the processing plumbing handles non-human transaction cadences.

I've been mapping these micro-temporal volume shifts on my Substack to see how merchant terminals manage "dead air" capacity gaps versus sudden velocity waves. It turns out tracking that velocity metadata pipeline is a massive leading indicator for merchant portfolio churn before it shows up in macro financial data.

I open-sourced the data science model behind it (time-series-velocity-baseline) in a piece called "The Velocity Multiplier"—would love your perspective on how the physical network layer handles these shifting commerce paradigms!