How credit card rewards work

Taking a look at the business model of credit card rewards. Highlighting some key differences present in the USA, the UK, and Indonesia.

For the consumer, credit card rewards are great. Just by using a particular card to pay for goods or services, we can get the product we want, and additional benefits too. These rewards often come in the form of air miles - airline loyalty points, cashback, rebates or some other benefit.

If I pay with a debit card, a credit card, cash, or some other means, the retailer still gets the money. But specifically with a credit card the consumer may also gain extra perks. So how does this work? Rewards are possible due to the business model of card payments.

Wherever card payments occur, the same core business model is in play. But when it comes to rewards, some markets are more lucrative than others. Regulations affect rewards, and individual markets vary. It’s interesting to look at examples of how countries rewards markets have evolved differently, but firstly, let’s understand the business model that makes credit card rewards possible.

What’s the business model?

We can separate the business model for credit card companies into four distinct revenue streams:

A fixed annual or monthly fee, sometimes known as a membership fee.

Interest fees.

Interchange fees.

Ad-hoc fees, including foreign exchange fees, when a card is used abroad.

The most important of these fees for our discussion is interchange. Interchange fees vary between countries, but interchange is present alongside every transaction. One of the most straightforward explanations interchange can be read in the post Interchange in 1,000 words on Notes by Matt Brown:

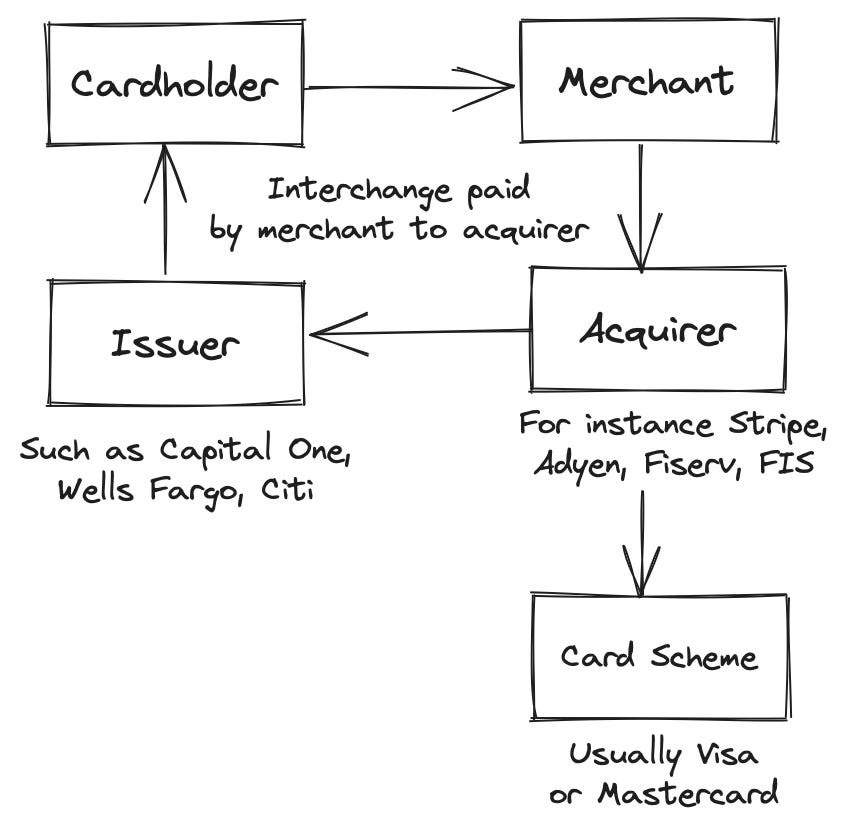

Merchants pay a small fee to accept card payments. This fee is split among the intermediaries that move the money from your account to the merchant. Those key intermediaries are the:

issuer, which markets to cardholders, issues them cards, and manages their accounts

acquirer, which enables merchants to accept card payments

scheme, or network, which connects issuers and acquirers, and sets rules for the transactions between them

We’ve mentioned card acquirers in previous posts, such as when looking at how software disrupts payments, or how banks can be a payment processor.

The acquirer is the one who charges the merchant, and they deposit to the merchant’s bank account the transaction value minus the processing fee. The acquirer keeps a margin, and sends part of the processing fee to the card issuer and the card scheme.

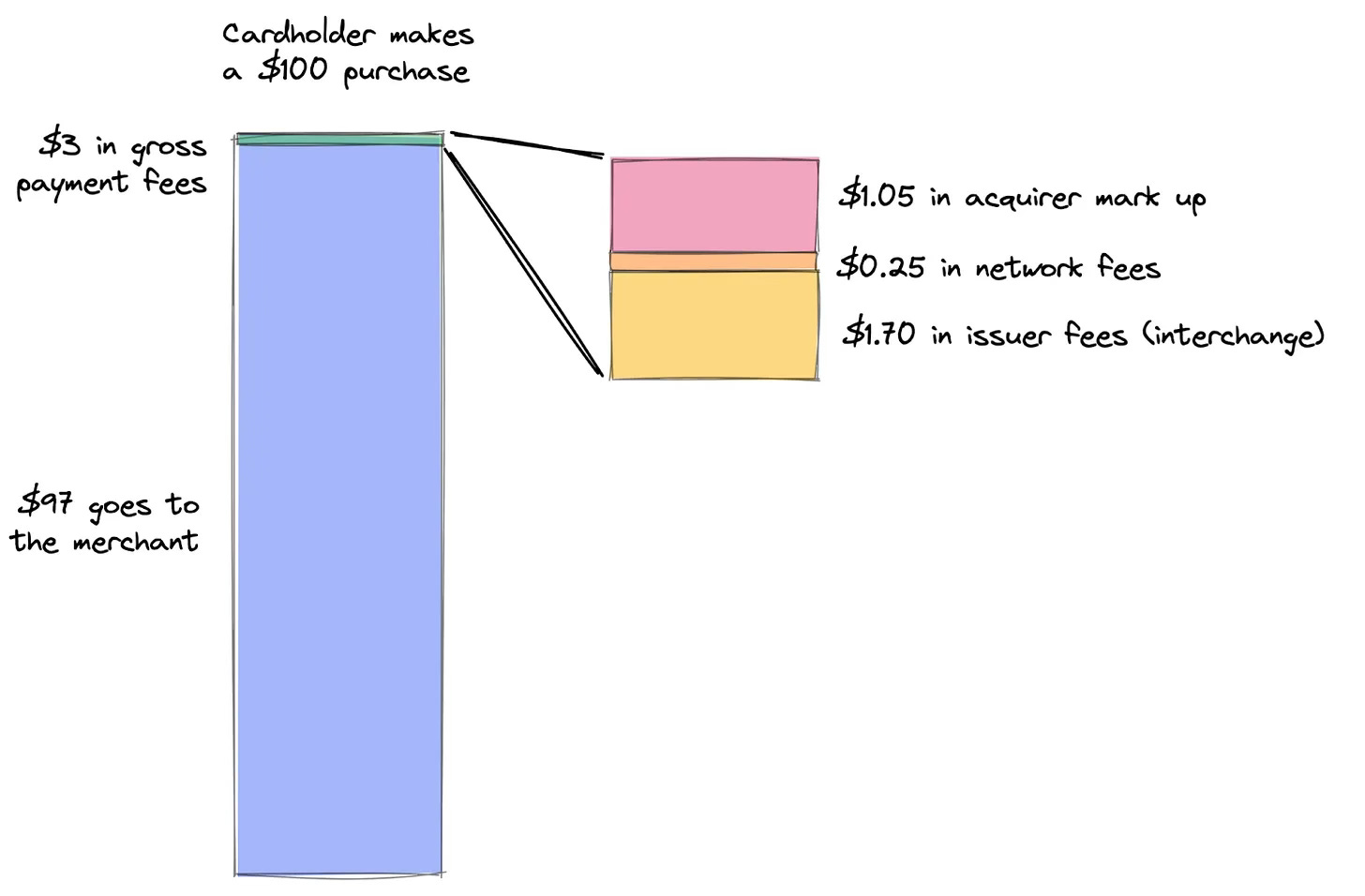

In the below example of a $100 purchase, the merchant is charged 3% for payment processing - so they receive $97 into their bank account. The card acquirer takes their margin of %1.05, the card network %0.25 (usually Visa or Mastercard), and the card issuer takes %1.70. It’s clear that the largest share of the revenue on a card payment transaction is the interchange fee.

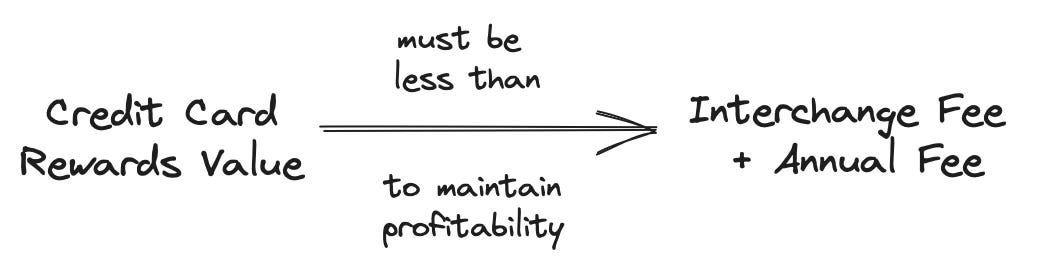

The value of the interchange fee allows card issuers to pay rewards to their customers.

Provided rewards paid are less than interchange and operating costs, then at scale, card issuers can maintain profitability. This is to oversimplify, given there are other fees that may be charged. However, the important point is that the value of rewards paid must be lower than the interchange fee.

Additionally, if the interchange fee is too high, there is always the risk that retailers stop accepting card payments. This is yet to happen, but there is a balance. As the Economist recently highlighted:

Cards have also become adept at retaining customers through juicy reward points, tied to everything from beach holidays to airline miles. These are funded through transaction fees which may seem hefty, but are not so big as to persuade retailers to refuse to accept cards.

The United States - big rewards

In the United States (US) interchange fees are complex. The full range of interchange fees are publicly available on the Visa and Mastercard websites. But you may have to search on Google to find them, as they are not so easy to find. Interchange fees can differ based on the type of business the card is used at and the type of card itself.

For instance, on a Visa consumer credit card, interchange fees can range from 2.10% to 2.60% when used at a restaurant. When cards are used at a supermarket, interchange fees can from 1.15% with an additional flat fee of $0.05 up to 1.40% with an extra $0.05. Different sectors incur different fees. If a card offers little or no rewards, then the interchange fee will be at the low end. Cards that offer the highest rewards will incur an interchange fee at the high end.

Business will pay a higher fee to accept cards with a higher rewards payback to the cardholder. This has led to some complaints that cardholders who pay with less lucrative cards are subsidising those who pay with higher earnings cards.

Most credit card companies prefer to offer their most rewarding cards to customers with a strong credit score and a higher-than-average income. As someone works longer, and their salary rises, more cards open up to them, and more options.

The below video reflects this, showing a ranking by tier of various credit card programs. These views are just the opinion of the creator, but it is true that there is a ladder of rewards. Many people find that it’s not easy to transfer a credit score across borders, so new immigrants to a country will often need to move up the ladder gradually.

Credit card rewards are a big business. Approximately nine out of every ten credit card purchases are made with a rewards card. The sheer scale can be pretty astonishing. For instance, in a recent investor presentation, Delta Airlines stated that almost 1% of US GDP flows through their various rewards cards. According to Skift, spending may be around the $250bn mark on Delta cards.

Some studies have highlighted that the average reward benefit on a credit card transaction is equivalent to 1.30% of the transaction value. According to Deloitte the average total benefit that a cardholder receives from a rewards account is around $170 per annum.

For a small annual fee, cards such a the Chase Sapphire Preferred credit card provide a smörgåsbord of benefits. Websites such as The Points Guy are on hand to help consumers maximise their benefits and get the best offers. With all this, it’s no surprise that many consumers are so focused on maximising their rewards payback.

The United Kingdom - small rewards

Compared to the US, the United Kingdom (UK) is not a great credit card rewards market. A decade ago, this was quite different. There was once a wide array of rewards cards offering various benefits to consumers.

All that changed with regulation. The Payment Service Directive 2 (PSD2) capped interchange rates in European Union (EU) countries at 0.20% for debit cards and 0.30% for credit cards. The regulation came into force in January 2016, and from that time, the rewards cards available were either gradually withdrawn, or the benefits reduced over time. Since the UK left the EU, the rules have stayed in place.

This is in line with our earlier statement that it is the value of the interchange fee which allows card issuers to pay rewards to their customers. As regulation pushes the interchange fee lower, card issuers must reduce their rewards offerings to remain profitable.

Whilst consumer interchange fees were capped, corporate cards were not. Today it’s still possible to get 0.5% cashback on a business debit card from Wise, and 1% on a business credit card from Capital on Tap. As well as exempting corporate cards American Express (Amex) cards were also not included in the regulation.

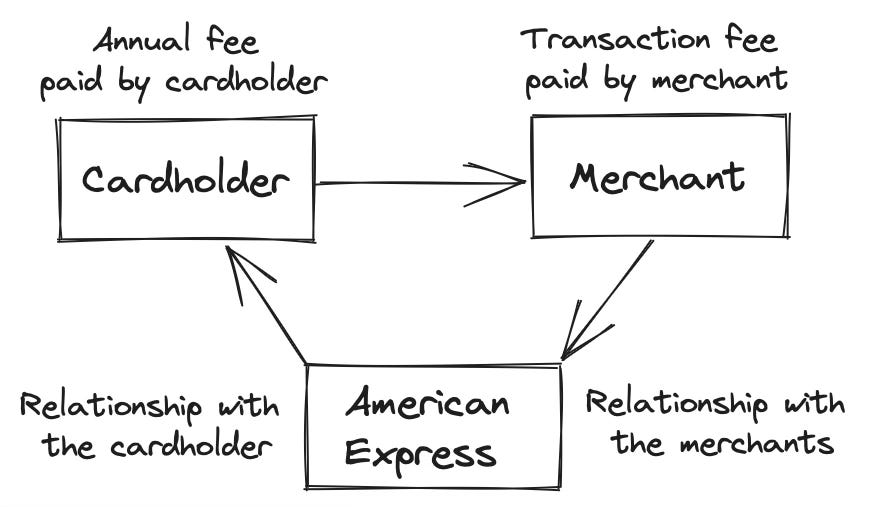

Amex were excluded from the PSD2 regulation as they are considered to be a three party, as opposed to a four party model - seen in the earlier diagram. Technically, in the three party model interchange is not charged. But a processing fee, or transaction fee, akin to interchange is still charged to merchants by Amex, and this is used to fund credit card rewards to the benefit of consumers.

Analysis by Money Saving Expert shows that all of the top rewards card in the UK are Amex cards. Non-Amex rewards cards are almost non-existent, but the Virgin Atlantic Reward+ card may make sense if you don’t mind paying the annual fee. But overall in many cases, consumers who value rewards prefer to use an American Express card, to make the most of the benefits on offer.

Now some new options and business models are now emerging in the UK. Yonder is a start-up focused on improving the credit card experience. They are giving those who want a rewarding credit card more options than looking to Amex. Yonder curates a selection of experiences each month, such as restaurants, bars, and wellness activities. Every pound spent on a Yonder card accumulates points, which can be redeemed at the recommended experiences each month.

As well as a monthly fee and earning from interchange, Yonder’s business model also has an additional element. The other part is revenue from enabling in-app marketing. By curating venues for its cardholders, Yonder can drive footfall and generate extra income for the businesses. Businesses can track the incremental spend from Yonder cards, which may result in a revenue share. Currently, Yonder only recommends activities in London but will expand to other cities soon.

Indonesia - different rewards

Indonesia is a country of 278 million people with a rapidly expanding economy. It’s a country fast becoming a key player in emerging fintech and payment solutions. The major banks in the country offer a variety of credit cards with rewards such as cashback, air miles, and even discounts on utility bills.

On a recent visit to Indonesia, I noticed something I haven’t seen in Western countries. Many places, especially restaurants, advertise specific discounts for cardholders who pay with the card of a particular bank. These offers are usually time-limited and can range from a rebate of around $5 to a discount of 20% on the total bill.

Indonesia is a country where most card acquirers are themselves large banks. When the card acquirer and the card issuer are the same organisation, there is the option to absorb the interchange fee from a transaction. These transactions are known as “on-us” transactions. The interchange fee saving can be used to offer a discount to the card holder and drive business to the merchant.

From a consumer perspective, on the one hand, this is a positive. But on the other hand, it means that many cardholders end up with a wallet full of cards from various banks. This arrangement allows customers to take advantage of merchants' discounts based on the card used. It’s a case of payments and credit card rewards varying across markets and cultures.

Thanks for reading Payments Culture!

Note that views expressed on this Substack are my own and do not represent any other organisation. Also nothing I say should be taken as investment advice.

Digital payments may be convenient; but they are a tool of autocratic technocracy intended to increase surveillance and control of our lives. Digital payments can be denied by the "system" for whatever reason, while cash payments cannot. Digital payments are the chains of slavery. The Chinese are already enslaved. If the Japanese know what is good for them, they will choose to continue using cash.