How India's Digital Public Infrastructure (DPI) is changing payments

India's tech stack is building innovative payment solutions at home and abroad

In the 2020s, infrastructure is key. From high-speed broadband to high-speed trains to renewable energy infrastructure. Every country is developing their infrastructure at pace.

Sometimes, national infrastructure is built solely with in-country expertise. Other times, external entities such as foreign governments or international institutions may offer financial or material support.

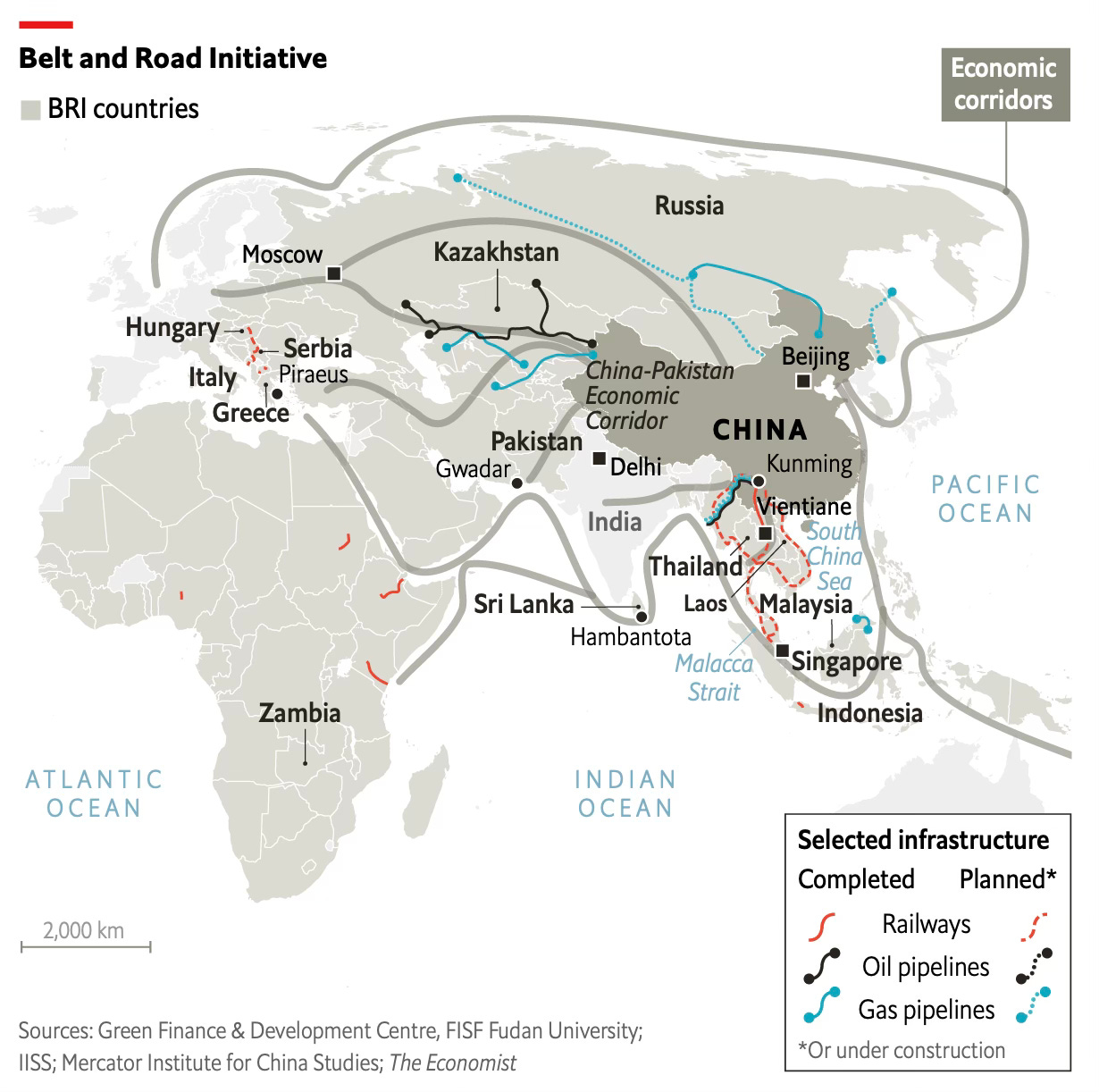

China's Belt and Road initiative is a famous example of infrastructure development with outside help. So far, over 150 countries have signed up to Belt and Road initiatives. Some estimates put the combined value of all Belt and Road projects at over $1 trillion.

With Belt and Road, China has built alliances, particularly in developing economies. And Chinese companies have been able to gain a foothold in new markets. There are criticisms of Belt and Road, yet recipient economies have been able to build bigger and faster than they would have otherwise.

In April 2023, the Vientiane-Kunming railway line opened. Connecting the capital of Laos to one of the most import cities in South-Western China. Laos would not have had the resources to build high-speed rail without Chinese help.

And Indonesia has recently opened a new high-speed rail line with Chinese help. Reducing the journey time from Jakarta to Bandung (the 3rd largest city) from more than 3 hours to less than one hour. Railway diplomacy has been a big success.

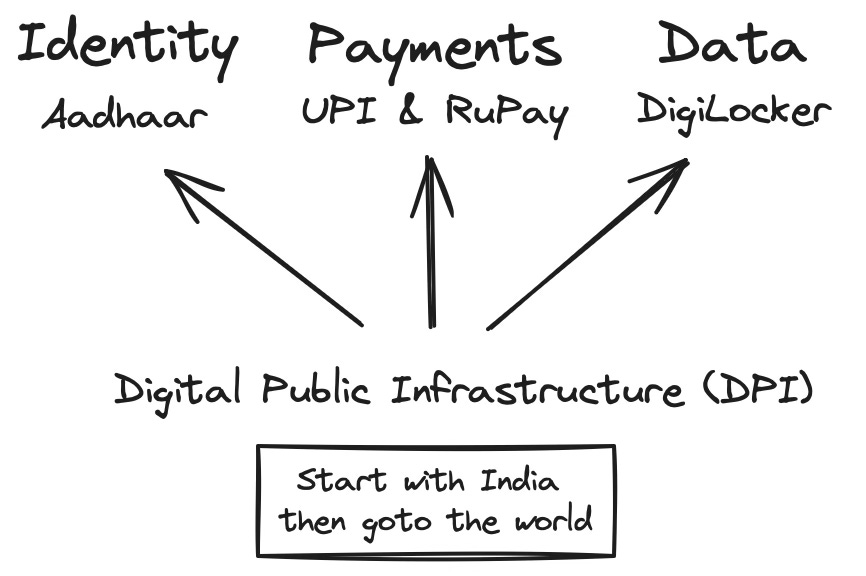

We can make a comparison here between India and China. While China's Belt and Road has focused mainly on physical infrastructure, India's initiative is Digital Public Infrastructure (DPI), which is centred on software and digitalisation.

Partly, this difference in emphasis reflects the constraints of each nation. China has the economic clout to build overseas, whereas India's economy is earlier in its development. However, India is a renowned software hub with deep expertise in digitisation that can be used to revolutionise digital technology.

The concept of Digital Public Infrastructure (DPI) is India's model of scaling infrastructure. There are three key pillars:

- Identity

- Payments

- Data

Let’s take a look at each of these, how they work, and how they scale.

Scaling Identity

In Western countries, identity (ID) isn't a problem. We can easily prove our identity with a driving license or a passport. Unfortunately 850 million people in the world have no ID at all, and an ID is a gateway to opening a bank account, getting a job, of accessing other public services.

Thanks to Digital Public infrastructure, nearly all of India's population is now part of a digital identity system called Aadhaar. Aadhaar provides a 12-digit unique ID number linked to biometric and demographic data, and is used to access various services in the country.

Aadhaar has inspired MOSIP (Modern Open Source Identity Platform). Born from the International Institute of Information Technology in Bangalore, MOSIP has been a success. The organisation has been able to deliver this pillar of DPI to markets outside of India.

One example is the Philipines. So far, it's estimated that 90% of the eligible population of the Philippines has registered for MOSIP. The solution has yet to go live, as the focus has been on getting people signed up, with the next stages to follow soon.

Scaling Payments

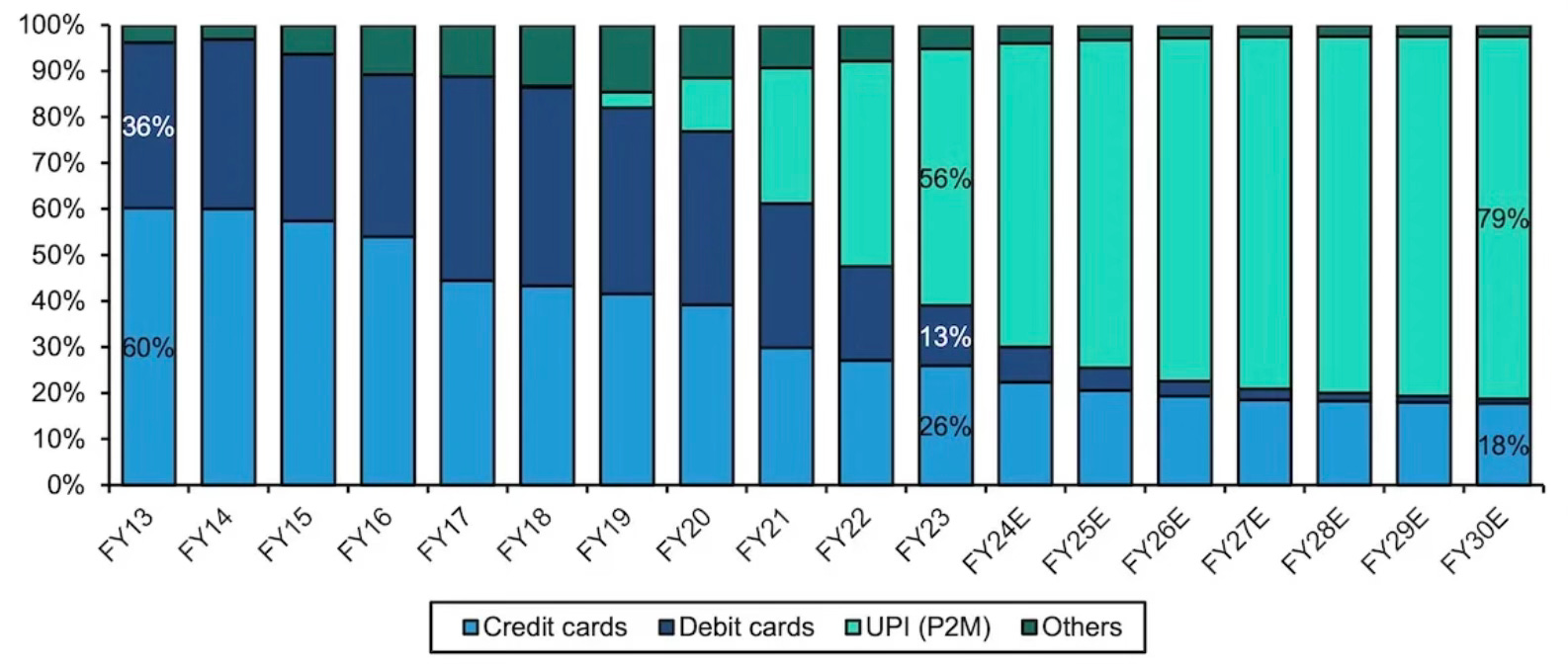

DPI's payment initiatives have been successful by most applicable measures. The National Payments Corporation of India (NPCI) was established in 2008 as a public-private body. The NPCI runs RuPay, a domestic card network for Indian banks, which has issued more than 750 million cards so far. RuPay claims to be up to 40% cheaper than international payment cards.

As well as RuPay, NPCI has developed Unified Payments Interface (UPI), an instant payments system. The closest comparison in Western markets would be a real-time Open Banking payments system (direct account-to-account payments).

UPI has snowballed since launching in 2016. In July 2023, UPI processed over 10 billion transactions - as a comparison, there were approximately 2 billion card transactions in the UK in the same month. The UK has a far smaller population than India, but it's a mature payments market, so this shows how big UPI has become in quite a short time period.

UPI is accessed differently from card payment facilities. Banks provide the UPI infrastructure, and consumers access UPI through consumer-facing apps. Usually, this entails scanning a QR code to start a payment app when shopping at a merchant.

The three largest apps cover approximately 90% of the market - PhonePe, Google Pay and Paytm. Unlike credit card payments, which incur a percentage fee per transaction, a vast majority of UPI transactions have no fee. Merchant fees were abolished in 2020. This lack of merchant fees has meant UPI-focused companies have struggled to make money so far.

Recently, merchant fees have been reinstated for some transactions. But these new rules only cover a low single-digit percentage share of the transactions. Thus, UPI apps have developed other business models to compensate for the lack of a merchant fee. Advertising in app, rental charges for hardware, or the provision of loans have all been utilised to some success.

PayTM is one example. They were the largest Indian IPO when they entered the public market in 2021. So far, it has been a hard road, with the company making losses every year. Their latest financial results presentation states:

Indian merchants’ unique features and pricing requirements warrants innovative product launches. We are focused on solving this by launching various types of Soundboxes and Card machines and other devices, backed by a large distribution and service network… Our focus is to expand credit offerings, which will help consumers and merchants find suitable product, in partnership with our lending partners… We are enabling merchants to offer deals on Paytm app which drives customer engagement, as well as consumer traffic to the merchants.

The company has had to innovate, given the revenue models available, and regulatory landscape in India. While the company is still making losses, losses have lessened recently, and the company will likely become profitable in 2024.

Scaling Data

The data pilar of DPI allows the storage of key personal data, such as a user's Aadhaar card, driver's license, and medical documents. These are stored within a database called Digilocker and can be shared or authenticated with third parties.

Some have pointed out that forged or other inauthentic documents could be stored in a user's DigiLocker. To some extent, such a system will only be as good as its users. But DigiLocker links to a user's Aadhaar number, which connects to a user's biometric information - which helps improve reliability.

The Indian government has mandated that all public agencies should adopt the service, and documents can even be setup to be accessed directly from WhatsApp.

At this time, more than 175 million Indians are using the DigiLocker service. As well as personal accounts, earlier in 2023 DigiLocker was also made availible for businesses. The connection of DigiLocker to businesses is something which will help fintechs scale more effectively, as sharing verified documents will now be much easier.

Taking India’s Payments Expertise Overseas

The success of DPI's payments pillar has opened up opportunities for the NPCI to expand abroad, and offer expertise to other countries. The principles of DPI can be utilised to build and support new card schemes in markets outside India.

Card schemes are often essential in the world of payments. They are the organisations that connect banks and payment processors. Through card schemes - sometimes known as card networks - transactions take place all around the world at the point of sale.

Banks choose to be a member of a card network so that their cardholders can pay in a wide range of locations. For instance, if a card is part of the Mastercard network, it can be used to buy goods worldwide, wherever the Mastercard logo is displayed.

The most well-known global card networks are Visa, Mastercard, and American Express. As we saw earlier, some countries have developed their own domestic payment card network - RuPay in India is one such example. Additionally, ELO in Brazil, Mir in Russia, and Troy in Turkey would be other examples.

It was recently announced that:

The United Arab Emirates is to establish its own domestic card scheme in a bid to encourage strategic independence from the Visa/Mastercard duopoly.

The Central Bank of the UAE (CBUAE) and its subsidiary payments infrastructure provider Al-Etihad Payments are to develop and implement the Domestic Card Scheme (DCS) in partnership with NPCI International Payments Ltd (NIPL), which led the development of India's RuPay card scheme.

A Press Release from the Indian Ministry of Industry and Commerce added further detail:

The DCS will aim to bolster financial inclusion, support the UAE's digitization agenda, increase alternate payment options, reduce the cost of payments, and enhance the UAE's competitiveness and position as a global payments leader. The partnership aligns perfectly with NIPL's mission to offer its knowledge and expertise to assist other countries in establishing their own cost-efficient, and secure payment systems.

The DCS solution is based on the principles of sovereignty, speed to market, innovation, digitization, and strategic independence. The DCS solution provided by NIPL consists of a RuPay stack and value-added services like fraud monitoring services and analytics.

India's world-renowned Digital Public Infrastructure (DPI) is driving massive transformation in the payment space. DPI framework includes digital identity, digital payments, and digital data exchange layers - a combination of these three is the force behind the fintech revolution in India.

Some key points are noted in these announcements. Visa and Mastercard are publicly listed companies based in the USA, subject to US rules and regulations. In most cases, this is fine, especially in Western economies. In fact, countries such as Germany have seen their domestic card network decline in favour of Visa and Mastercard.

However, some countries want to build their own infrastructure and control their own card network for domestic payments. The ability to set fees and customise a solution for local needs is seen as a positive.

Also, data sovereignty has become a key driver for digital infrastructure. Can a country store its data, including that for payments, within its own borders? This may be especially important in a world where geopolitics and business are converging more and more.

The Impact On International Card Schemes

Local card schemes and domestic payment methods can significantly impact the payments industry at large. In India, the growth in UPI has led to a decline in card transactions, with debit card payments down 15% year over year.

Mastercard was banned from signing up new customers in India for almost a year from the middle of 2021. This was due to non-compliance with India's Storage of Payment System Data regulations. Still with Mastercard, their CFO, Sachin Mehra, recently commented:

It is an incredibly painful experience for ecosystem participants who all end up losing money as part of that proposition

Many in India argue that UPI will in time allow companies to find suitable business model(s) to be sustainable, and importantly broader goals are at stake here. DPI is a set of principles focused on digitisation and financial inclusion more than revenue maximisation - at least for now.

International organisations can still benefit, as domestic payment schemes can often be used abroad. For instance, RuPay cards run on the Discover payments network when used overseas - card networks will compete to be the international network of choice. UPI will become interoperable with other payment systems over time - with the exact solutions differing depending on the country.

The latest tailwind for the international card payment schemes in India is a regulation in effect from the 1st of October. This will allow customers to select the card network of their credit or debit card. The options are Visa, Mastercard or RuPay. Will cardholders opt for the domestic champion? Or for the well-known international card brands?

Thanks for reading Payments Culture!

Note that views expressed on this Substack are my own and do not represent any other organisation. Also nothing I say should be taken as investment advice.