How software disrupts payments

Mobile technology and app-stores transform distribution for payments companies

Today we have an on-demand economy and can do almost everything we need from a mobile phone. We use phones to book a taxi or hotel. We can check up-to-the-minute sports scores. And many of us do our day-to-day banking on our mobile phones as standard.

This trend for apps, for a software-first world, has grown massively since Marc Andreessen declared, over ten years ago, that “software is eating the world”.

Now software is seeping into every aspect of our lives, especially with the growing interest in Artificial Intelligence (AI) and big data, we will become more and more aware of how software impacts us. Everything is becoming software.

Especially in the era of app stores, the software has zero marginal cost. In other words, once an app is developed and launched, the distribution cost for each new user is close to zero. With app-based businesses there is no physical store and no physical product; this means software-based businesses have some unique characteristics.

Companies traditionally have had to incur (up to) three types of marginal costs when it comes to serving users/customers directly.

The cost of goods sold (COGS), that is, the cost of producing an item or providing a service

Distribution costs, that is the cost of getting an item to the customer (usually via retail) or facilitating the provision of a service (usually via real estate)

Transaction costs, that is the cost of executing a transaction for a good or service, providing customer service, etc.

The world of payments traditionally did operate in this way, with the marginal costs noted above, when most payments required Point of Sales (POS) hardware. This was the nature of payments in earlier times.

In contrast, a new model is changing things, especially due to software-based payment solutions. Let’s look at how we got here.

Card acquiring in brief

For many decades, card acquirers were part of a bank. They provided businesses with the ability to accept credit and debit transactions at the point of sale. This card-acquiring capability formed part of a business banking relationship. As well as card acquiring a bank provided a current (checking) account, credit cards, loans and other products and services such as insurance.

These original card acquirers were typically concerned with Card Present payments (payments taking place in an in-store retail environment). Facilitating in-store payments required the provision of Point of Sale (POS) hardware.

Card acquirers needed a wide range of resources to support POS payments. For instance, a sales team to go out and meet large clients, sign contracts and show the hardware in action; specialised staff to integrate and provide project management expertise; a call centre to handle technical issues, and make outbound sales to smaller less complex clients.

In short, for a long time, being a card acquirer required a wide range of infrastructure and personnel. These companies eventually got around to providing online payment solutions, besides in-store payment solutions. However, their focus remained on card present payments.

With the growth in e-commerce, a new wave of acquirers entered the market in the 2000s and 2010s. Companies such as Adyen, Stripe and Checkout.com focused on APIs. They enabled companies to integrate into a broader range of payment types and service a comprehensive range of geographies. This was the internationalisation of payments on a scale not seen before.

Allowing businesses to offer their customers Visa and Mastercard as payment had been enough up until this point. But this new wave of acquirers offered more. PayPal and other payment types become essential. In Europe, bank-to-bank payment schemes became popular on a country-by-country basis. For instance, SOFORT in Germany and iDeal in the Netherlands were as important, or even more important than card payments, in order to grow in these markets.

In the early 2010s, e-commerce took off in the UK, as did contactless payments. Particularly notable was the London 2012 Olympics. One of the main sponsors, Visa, ensured that contactless payments were accepted at all venues.

Contactless payment volumes grew year on year and the rise of contactless payments in allowed traditional acquirers to keep growing in the card-present area.

The second wave of acquirers continued their focus on e-commerce. They started to provide physical POS solutions only much later when some large clients needed a full multi-channel solution.

The strategy worked, as e-commerce brought higher margins than card-present payments. And the second wave of card acquirers were very successful. Becoming multi-billion dollar companies and surpassing many of the original acquiring banks’ parent companies in valuation.

A new change is happening, at this time in 2023, allowing businesses to accept payments is becoming a matter of software, or, quite simply, an app.

There’s an app for everything these days.

Reflecting that we may be at the start of another era of payments transformation, Akash Bajwa has written:

Adyen, Stripe, Braintree and the remaining companies that make up the first cohort of modern, native acquirers/processors have organically reached a scale and maturity that leaves them vulnerable to the classic innovator’s dilemma.

These innovators will be software first and take us from the era focused on e-commerce, in which the second-wave acquirers dominated, to a new era of software-based disruption. Some will adapt but new entrants will also enter the market.

The emergence of payments as software

Key trends have enabled the rise of payments as software. The rise in app stores for one. But also improved mobile devices and the growing prominence of contactless payments. Nowadays, we can tap a card on a POS rather than need to insert a card into a POS, which makes payments quicker and easier.

Each country has its own limit for contactless payments, for instance, £100 in the UK. Additionally, Apple Pay and Google Pay allow High-Value Contactless where the use of biometrics permits an amount much higher than the standard limit.

Of course, some markets have been ahead of others when it comes to contactless. As mentioned, the UK has been a leader in contactless payments for over a decade; the US has been recently catching up. But despite the difference in the population and market size for card payments, it took until 2022 for the US to overtake the UK:

The US reached 28% [contactless] penetration and saw more than 1 billion tap monthly transactions for the first time ever in July, surpassing the UK as the largest country for Tap to Pay transactions and this is nearly double the number of transactions from last year and more than 5 times the number of transactions from two years ago.

The growth is impressive year-on-year, but the 28% contactless penetration is low (assumed to mean the percentage of cards issued that are contactless). According to Mastercard, more than 100 markets globally now have more than a 50% contactless penetration rate.

We can see from the below video that in the US, only 55% of retailers currently offer contactless payments. But now, transit systems are embracing contactless payment technology, including the New York Subway.

Enabling public transport with contactless is a good sign. London was a prime case of how changing habits with people’s daily commute can change habits. Consumers will soon expect the same in-store payment experience as they get on public transport.

The most significant change to widen the reach of contactless payment is at the end of the video. This is SoftPOS (Software Point-of-Sale), sometimes known as Tap to Phone technology.

SoftPOS is a technology mentioned in the previous post on the topic of sustainability.

This technology can turn a standard Apple or Android device into a Point of Sale terminal by using the phone's NFC. This allows companies to build contactless payment functionality into any app.

With SoftPOS a small business can download an app, and start taking payments within minutes. So no need to wait to get a physical POS machine to be delivered before transacting anymore.

Square (now part of Block) has been an important innovator and link between traditional POS and a new generation. Square pioneered a new form of smaller and lighter POS devices and the device pairs via an app on an Android or Apple phone to set the payment amount.

Before Square, businesses often had to pay a monthly fee per POS device, usually £20 or more per month in the UK. This was a way of amortising the cost of buying the POS hardware with some margin added on top. With Square offering a card reader for a flat fee of £50 or less, it’s hard to justify paying an acquirer a monthly fee for a card machine in many cases at least.

Software opens new possibilities

The fundamental change is that companies can now enter the payments market by building an app. They do not need to be a payment gateway, processor or card acquirer themselves. But they will need to connect to one or more of these parties to launch their solution.

The emphasis is on the customer experience and owning the customer relationship. With a software-based solution, onboarding can be streamlined and businesses can start taking payments within minutes. Digital ID documents can expedite processes which may have taken days or weeks in the past.

With today’s app stores, companies can easily distribute their software to smartphone users An extensive sales function that the first-wave card acquirers may have needed is now a choice, not a need. Instead, online channels such as social media can drive app downloads and traditional marketing techniques such as “refer a friend and you’ll both get £5 credit” can be used to get users to try out the solution.

Square themselves have recently started offering SoftPOS, Tap to Phone, in some markets. Square has been advertising the solution to users on Facebook and Instagram. This allows users to click straight to the Google Play or Apple App Store, download and start taking transactions.

Thus Square is among the first movers in this category of disruptive software providers. They offer acceptance of card payments with small hardware devices, SoftPOS, and other services. Other services include gift cards, loans to businesses, and Buy Now Pay Later (BNPL).

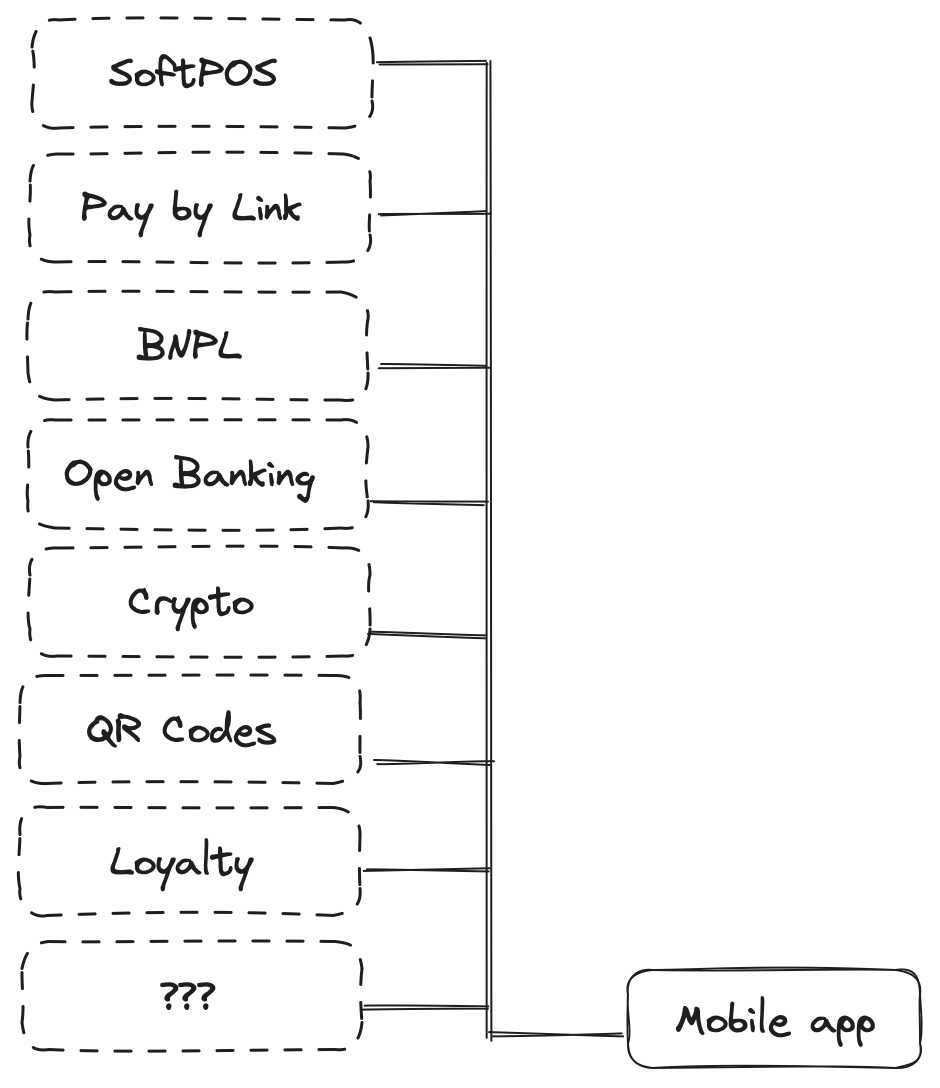

A key point in this new era of payments as software is that card payments may be only one solution built into a payments stack. SoftPOS may be a good starting point for users to download an app and start taking payments. Or Account-to-Account (Open Banking) payments may be a good entry point.

Over time extra solutions can be added, such as pay-by-link, QR code payments (for example, to enable China’s WeChat and AliPay, or India’s UPI), BNPL etc.

The preferences will depend on the business needs of merchants in specific markets.

Merchants’ needs are evolving... Value-added services like credit solutions, BaaS, front-end and back-end software are becoming increasingly important dimensions in payment processor shopping.

Those who succeed will provide a solution that best appeals to target users, and business segments, with a keen focus on user experience. Trends such as embedded finance will enable a greater variety of options in moving from just providing payments to providing a wider array of financial services as needed.

Payments will continue to be complex in the background. The providers who succeed will stay ahead of the game and make it convenient for businesses to operate and scale.

It’s likely that many of these software disrupters will not be payment processors themselves, at least not to begin with. The back-end processing of transactions may be seen as a commodity.

Those who succeed, over time, may decide to become a Payment Facilitator (taking on some of the roles of the acquirer), a payment processor or even an acquirer themselves. It will depend on what makes business sense. This has been the approach of Square in moving further into the payment stack over time.

With software, a modular approach will be standard. For each component, a decision can be made on whether the solution should be built in-house or connected to another provider. There will be a mix of providers who will go to market directly or provide a white-label approach.

Most apps will connect to the APIs or SDKs of other SaaS (Software as a Service) providers. This will be the norm for SoftPOS and Account-to-Account payments. The ability to connect solutions and build an overall payment stack with the best combined merchant experience will be key. No need to own all parts of the solution, rather focus on scaling and delivering a superior user experience.

Thanks for reading Payments Culture!

Note that views expressed on this Substack are my own and do not represent any other organisation. Also nothing I say should be taken as investment advice.

This is a fantastic write up! Thanks for the plug Matt!