Polygon is ready for agentic commerce

CEO Marc Boiron on why legacy payment infrastructure wasn't built for AI agents, and what can best replace it

Welcome to Payments Culture!

This newsletter explores how money moves, around the world — and why it matters.

You can contact me on LinkedIn, Twitter (X), via email.

Agentic commerce is one of the key themes of the moment, and one that I’ll be returning to time and again this year on Payments Culture. Payments infrastructure is evolving fast and in this newsletter, Marc Boiron, CEO of Polygon Labs, makes the case that legacy rails are not up for the task of supporting agentic payments. He also makes the case for what can replace the legacy system. As with all guest contributions, the views are the author’s own.

The race to define agent-driven commerce is already well underway.

Visa, Mastercard, Stripe, and PayPal are all introducing frameworks designed for a world where software can search, compare, and transact on behalf of users. The scale of what this could become is enormous. Deloitte estimates that this shift could influence $17.5 trillion in global commerce by 2030, while McKinsey puts the opportunity at $3 to $5 trillion in orchestrated revenue.

There is no question that the demand is real and that serious capital and attention are moving in this direction.

What is less discussed is that the infrastructure these systems rely on was never designed for this model in the first place, and that mismatch is going to matter more than anything else.

Before getting into the infrastructure, it is worth being clear about how these systems behave. They are not emotional buyers. They do not respond to urgency, branding tricks, or scarcity cues. They optimize. A system managing spend will evaluate every option available, compare pricing and performance, and execute the most efficient outcome without hesitation or bias. Over time, that dynamic should compress margins and force genuine competition, which is ultimately a benefit for end users.

But that only happens if the underlying rails can actually support how these systems operate. Right now, they cannot.

Today’s payment infrastructure was built around human behavior. Identity verification assumes a person is present. Authorization flows assume someone is approving a transaction. Settlement cycles assume business hours. Fee structures assume transaction sizes that make sense for a human purchase.

Software does not operate within those constraints.

A system that is negotiating contracts, managing subscriptions, and executing usage-based payments across thousands of interactions per hour cannot wait for settlement windows to open, cannot absorb fixed fees on tiny transactions, and cannot depend on manual approval loops. When you try to run that kind of activity on existing rails, you do not get efficiency, you get friction at every step.

Efforts like Visa’s Trusted Agent Protocol and Mastercard’s Agent Pay are important signals that the industry understands where things are going, but they are still working within the limitations of infrastructure that was designed for a different world. Adding new layers on top does not change the foundation.

If the buyer is software, then money itself needs to behave like software.

Onchain infrastructure functions as the key unlock in a future of programmable, software-based agents participating in financial transactions. These systems need programmable, always available money that can be viable globally, instantaneously.

An onchain economy is the only viable solution.

Programmability means that payments are no longer just transfers but embedded logic. A system can enforce rules on how funds are used, trigger payments when conditions are met, automatically split revenue , and settle obligations without manual intervention.

Always-on settlement matters because these systems operate continuously and globally. Settlement needs to happen in seconds, not days, regardless of time zones or weekends. On Polygon, that already happens in roughly two seconds at an average cost of less than a cent.

Equally important is the ability to support microtransactions. When the cost of moving value drops to fractions of a cent, entirely new economic models become possible. Payments can happen per API call, per data request, or per unit of compute. These systems operate at a granular level, requiring a financial model that works with the same level of targeted precision.

But even with fast, low-cost settlement, there is a second problem that becomes impossible to ignore: fragmentation.

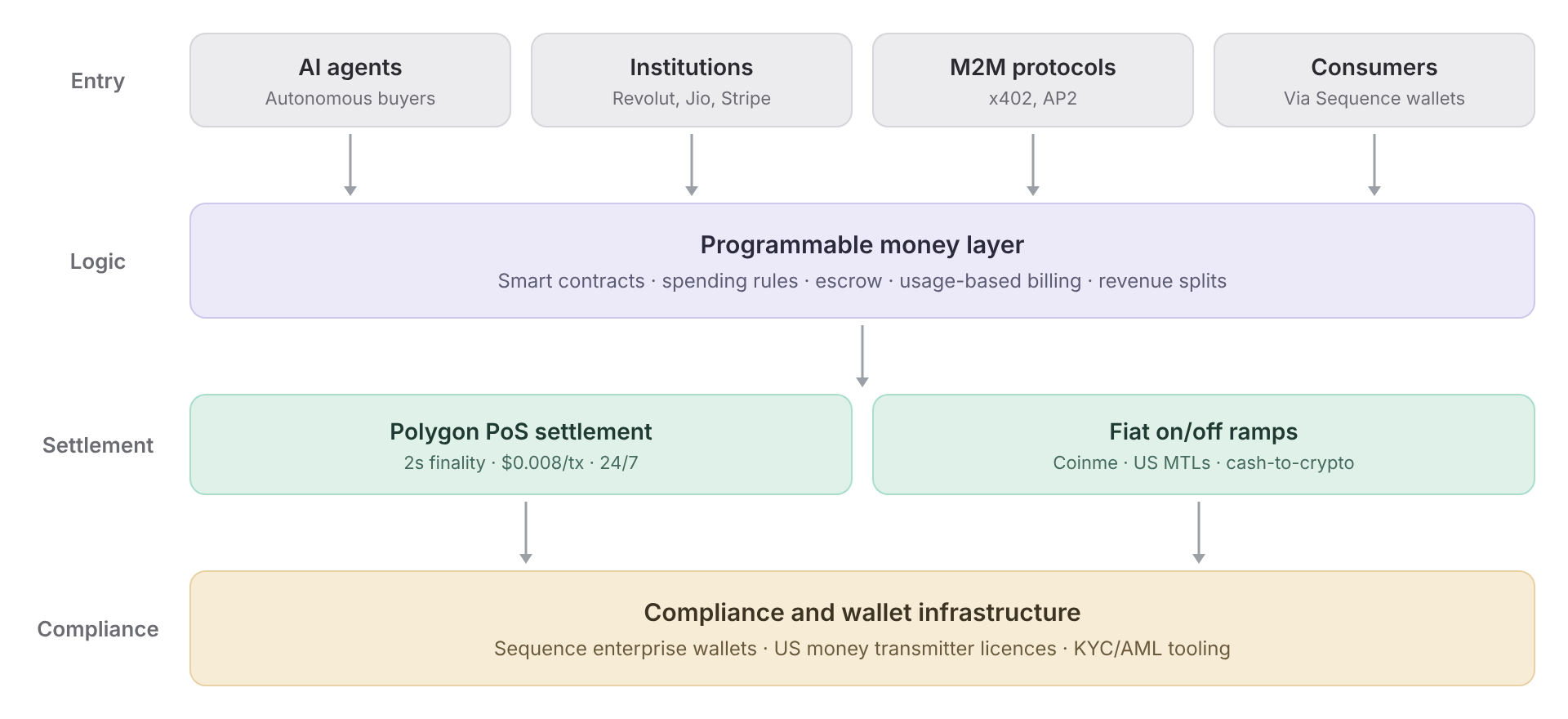

Today, most payment stacks — including those built around stablecoins —are stitched together from multiple providers. Wallets, fiat onramps, compliance tooling, routing, and settlement all exist as separate layers. Each integration adds complexity, cost, and failure points. For systems that need to operate autonomously across platforms and jurisdictions, that model does not hold up.

We’re building the Open Money Stack (OMS) for a unified, single API integration that will give institutions and AI agents everything they need for global money movement — all in one place.

The OMS unites wallets, fiat access, compliance, routing, and onchain settlement into one composable layer. Built-in compliance and crypto-wide interoperability help round out the OMS’s unique offering, delivering an enterprise-grade solution for existing and new institutions.

Instead of forcing companies to rebuild their systems, any enterprise can plug in existing workflows and upgrade underlying rails to always-on, programmable settlement that works in seconds rather than days.

If money is going to move the way information moves, then the experience needs to feel as seamless. Users and systems should not have to think about chains, liquidity, or routing. Background infrastructure, which we’re building with the OMS, should handle all this invisibly, allowing value to move across networks, currencies, and formats without friction.

Core aspects of the Open Money Stack are already live.

In February 2026, Polygon processed 493 million stablecoin transactions, the highest monthly volume recorded on a single blockchain. Over the course of 2025, total stablecoin transfer volume reached $932 billion, representing a 264 percent year-over-year increase. By March 2026, Polygon ranked first globally in transaction count, and stablecoin supply on the network grew to $3.28 billion, significantly outpacing broader market growth.

The participants driving this activity are not limited to crypto-native companies. Revolut, which serves 65 million customers, selected Polygon as its primary blockchain infrastructure for payments, trading, and staking, and has already processed more than $1.2 billion in volume. Jio Platforms is bringing blockchain-based payments and digital identity to over 450 million users through JioCoin on Polygon.

At the same time, early forms of machine-to-machine payments are emerging. Polygon recently recorded $1.2 million in weekly x402 transfer volume, reflecting systems transacting with each other in real time.

The $17.5 trillion opportunity will be captured by building infrastructure that aligns with how these systems actually function, where money is programmable, composable, and always available.

We’re making sure the Open Money Stack is ready to capture this opportunity, so money can finally operate like the Internet.

Please consider sharing this newsletter with a friend or colleague if you enjoyed reading this edition. If you are not yet subscriber please sign up below for a free or paid subscription.

Note that views expressed on this Substack are my own (or in this case the contributors) and do not represent any other organisation. Also nothing I say should be taken as investment advice.