Why you will get surcharged in New Zealand

And other things I learned in Aotearoa

Welcome to Payments Culture!

This newsletter explores how money moves, around the world, and why it matters.

Money20/20 in Amsterdam is coming up in less than two weeks’ time. If you’re heading to the show and would like to meet up to talk payments and fintech feel to send me a message.

You can contact me on LinkedIn, Twitter (X), via email, and with the below button.

One sunny afternoon this February in Auckland I strolled around the New Zealand Maritime Museum. Given its remoteness, New Zealand has an interesting seafaring history. The travel time getting to New Zealand illustrates this remoteness: it takes at least 24 hours of flying time from the UK, and at least one flight transfer; even the shortest flight from New Zealand to Australia, countries which are considered geographically close, is more than 3 hours. Landing in New Zealand really does feel like walking on the edge of the world. I had flown to Auckland from London via Qatar, which meant the second flight was 16 hours long.

I was still suffering from jet lag sauntering around the museum. With one too many delicious Kiwi coffees in my system (New Zealand and Australia argue over which country invented the flat white), I learned something interesting. New Zealand’s coastline was fully mapped only in 1855. Or should I say mapped in the Western sense with contemporary cartographic techniques.

The indigenous people of New Zealand, the Māori, generally passed information down through the generations via storytelling rather than writing. Maps such as the one that Māori Chief Tukitahua of Ōruru drew in 1793 are rare. This was drawn in extraordinary circumstances. The Chief had been taken from his home by the British, and he drew the map in chalk to show the location he wanted to be returned to. He was brought home by Lieutenant-Governor Philip King, a full nine months after he initially left.

Inland exploration of New Zealand was hastened during the 1850s and 1860s as the country underwent a gold rush. Immigrants arrived from Europe, and even from China, to earn their crust digging for nuggets. The population of the Otago region went from 12,000 to 100,000 in a matter of years. On this trip I realised that from a Western perspective New Zealand really is a very new country.

As a Brit, New Zealand feels like a place that can feel both slightly old fashioned yet at the same time very forward looking (compared to the UK). It’s not uncommon to find British quiz shows and soap operas on TV. In Auckland many homes can be opened with a 4-digit code entered on keypad, rather than a key, with the front door opening directly onto a busy street. Not something that would happen in London.

Other things I really like about New Zealand:

Taking the ferry from the Auckland suburbs to the central business district makes for a great commute. No ticket needed as I paid by tapping my contactless card.

New Zealand has really delicious food. Much of it is genuinely local and there’s great variety in cuisine. I had everything from delicious Japanese food to hearty pies — which are lighter and healthier than the UK equivalents.

Did I mention the coffee? Wellington in particular is known as a coffee hub with independent coffee places everywhere. The fact that every sip tastes so good adds to the quality of life.

Queenstown, in New Zealand’s South Island, is a unique place. It’s like a holiday resort, a mini theme park, and a picturesque alpine town all in one. In one day I rode a speed boat down a canyon, took a gondola up a mountain, and rode a luge down the mountain, before having a wine and steak dinner. Only in Queenstown.

As this Substack has to touch on payments sooner or later let’s move on to one of the slight negatives as a tourist in New Zealand. Even though this wasn’t my first trip to New Zealand, I’d forgotten about this aspect, and it surprised me.

You will be surcharged

The lunchtime before visiting the Maritime Museum I ate a delicious fish and chips in Auckland fish market — a short walk from the Museum. This was when I first noticed something that was going to be apparent throughout my two-and-a-half weeks in New Zealand. Surcharges for card payments — everywhere.

In the UK and EU surcharging consumer credit and debit cards is forbidden. You can still surcharge commercial or business cards, but in reality, most businesses — with some airlines the notable exception — avoid making this distinction.

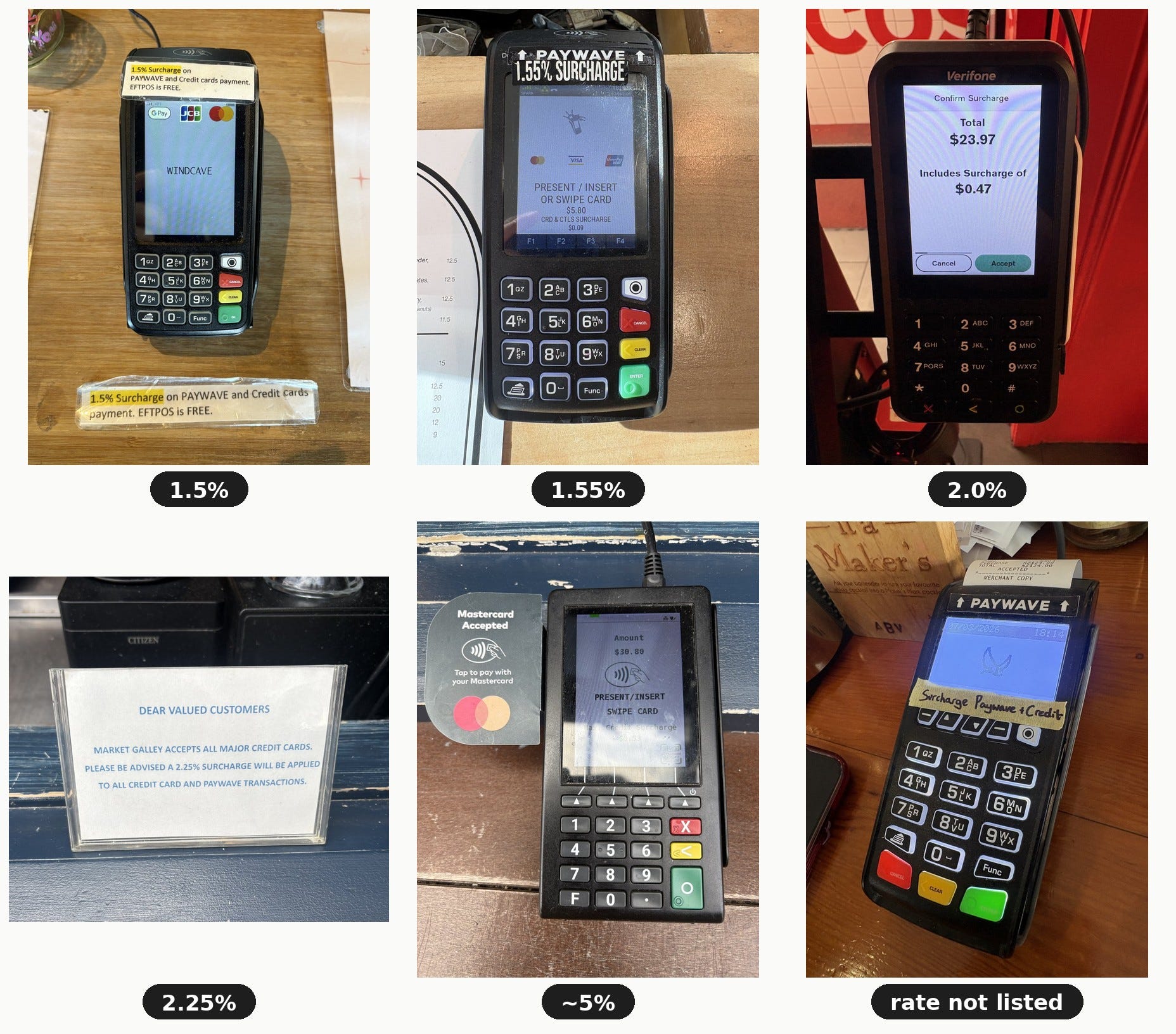

In New Zealand, you can pay with card everywhere, but almost every time I did pay with card I got hit with a surcharge of anywhere between 1.5% and 2.2% (with one outlier at 5%). New Zealand’s Payments Culture is unique and it highlights how the global and local come together.

Part of the reason for the surcharge stickers I saw across the country is historical. In the 1980s, as card payments started to take off, New Zealand’s financial institutions worked together to develop the EFTPOS payment system.

Some nuances of EFTPOS are as follows:

Users can choose between debiting their checking account or their savings account when using their EFTPOS card.

For merchants, accepting EFTPOS is almost free. There’s no percentage-based merchant service charge. The costs are limited to terminal rental and a small per-transaction fee.

Merchants got used to EFTPOS, and over the decades, the term became synonymous with card payments in general. Visa and Mastercard were available in New Zealand even before EFTPOS hit the market but the domestic system became the payment option of choice. The international schemes were used mainly for larger purchases or when travelling abroad. Due to the cost differential many small merchants refused to take Visa and Mastercard, and only accepted EFTPOS.

In the 2000s Visa and Mastercard developed debit card products to compete with EFTPOS. But the cost differential remained. Still today, many banks issue debit cards on the domestic as well as international scheme rails. If consumers wish to avoid surcharges they can use their EFTPOS card, but as a tourist this option does not exist.

Even for local consumers there’s been a downside to EFTPOS dominance — the domestic rail doesn’t offer Apple Pay. The surcharging norm on Visa and Mastercard has made Apple Pay and Google Pay more expensive for consumers to pay with. This inverts what we see in many other developed markets. In London tapping with Apple Pay is done without a second thought and mobile wallets are a growing consumer preference. But every time you tap to buy your coffee in Wellington you’ll likely pay 1.5%-2.2% more than if you’d used cash or your EFTPOS card.

The main fee component in card payments is usually the interchange fee. This is regulated at 0.20% for debit cards and 0.30% for credit cards in the UK and EU, but in other markets like the US, interchange fees of more than 2.5% are possible. Such fees are paid directly by merchants, by businesses who accept card payments, and in part make their way back to cardholders in the form of cashback or rewards of some kind.

The New Zealand government has regulated interchange, and recently tried to ban surcharging altogether:

From 1st December 2025 the interchange cap on in-person transactions went from 0.8% to 0.3% for domestic cards.

On the 1st May 2026 an interchange cap on foreign card transactions was introduced for the first time, capping fees at 0.7% for credit and 0.6% for debit.

Along with these interchange caps and cap reductions came a move to ban surcharging entirely. This failed in parliament earlier this year and looks unlikely to return to the table any time soon.

Although interchange fees are now lower, it doesn’t mean smaller merchants will see their bills reduce accordingly — in some cases, card processors may gain additional margin in the short term instead of passing it on to their customers.

The Commerce Commission, New Zealand’s competition and consumer regulator, estimates that there’s NZ$45m to NZ$60m in excessive surcharging each year over and above the actual cost of accepting payments. At least for now that’s getting pushed to consumers rather than absorbed by merchants.

Note: For a European comparator to EFTPOS something like Germany’s Girocard would make for a strong reference point in terms of consumer adoption and functionality.

Going beyond cards

Some tourists have to eat surcharges when spending in New Zealand. Other tourists literally get paid to shop. The biggest beneficiaries are Chinese visitors and residents.

The data helps tell the story.

In February 2026, coinciding with the Lunar New Year, more than 60,000 Chinese tourists visited New Zealand (this counts only mainland China passport holders and excludes passport holders from Hong Kong). The only country that had a higher number of visitors in February was Australia, which should be no surprise given the two countries have reciprocal arrangements to freely visit, live and work in each other’s countries. As well as the tourist visitors, over 30,000 Chinese citizens currently study in New Zealand, and there are around 150,000 Chinese-born residents in New Zealand, who either hold New Zealand passports or have permanent residency in the country.

In February 2026, depending on how you measure, between 4% and 5% of everyone in New Zealand was either a short-term visitor from China or a mainland-China-born resident. This represents a huge opportunity for retailers to tap into, but in order to do so they need to offer payment methods that Chinese shoppers are used to.

But it’s about more than just visitor numbers.

Chinese visitors spend an average of NZ$368 per day, which is second only to US visitors who spend $372 per day. Across an entire trip the average spend by Chinese visitors is $5,800. Meanwhile Chinese students in New Zealand spend an average of NZ$58,576 per student, much more than the international student average of NZ$45,776.

Accepting Alipay or WeChat Pay may be more costly than cards but given the spending capacity on offer it’s worth it. If merchants don’t offer these key Chinese payment methods then travellers and the diaspora may go elsewhere.

Aotearoa is what the Māori people call New Zealand, which is often translated as the land of the long white cloud. Although the name is poetic rather than meteorological, I was fortunate to be in New Zealand at the tail-end of summer and rarely saw a cloud in the sky. I’d learned that New Zealand is a fascinating example of the global and the local coming together. It’s a country of around 5m people, sparsely populated in parts, but holding a magnetic pull for visitors and newcomers from all over the world.

While locals still keep their EFTPOS card handy, I saw more signs offering JCB as a payment option than I do in London — that’s for Japanese travellers. Also far more signs offering customers the option to pay with Alipay or WeChat Pay in Kiwiland than I did when travelling in Taiwan (I’ll write more about Taiwan in a future post).

As I sipped my flat white in Auckland airport waiting to leave New Zealand I couldn’t help but think that as a Western tourist, understanding that you will get surcharged when you tap to pay is not a big deal. When life is this good it’s quickly forgotten. New Zealand may have an unusual Payments Culture but it’s one worth experiencing.

Thanks for reading this edition.

Please consider sharing this newsletter with a friend or colleague if you enjoyed reading this edition. If you are not yet a subscriber please sign up below for a free or paid subscription.

Note that views expressed on this Substack are my own and do not represent any other organisation. Also nothing I say should be taken as investment advice.

Payment habits are shaped as much by local infrastructure and incentives as by the technology behind them