How Apple Pay changed payments

Did Apple made payments cool?

One of the biggest changes in payments in the past 20 years was the introduction of Apple Pay. I can remember the day it was announced, in September 2014. It may seem strange to remember such a thing, but for payments aficionados it was a big deal.

Why was it such a big deal? Because Apple Pay accelerated contactless payments.

A personal anecdote highlights this. A few years ago my Mom was visiting me in London.

While in a cafe, I barely noticed it happen, but my Mom effortlessly paid our bill using Apple Pay on her Apple Watch. I hadn’t shown her how to do this, so I thought it was cool to see how someone from the Baby Boomer generation (born between 1946 and 1964) had embraced payments via a watch.

This highlighted to me the extent to which payments had become embedded into devices.

And to a large part, Apple Pay was the key factor in making this happen.

Going back to 2014. At this time Apple was behind the times. Every other major phone maker had NFC (Near Field Communications) in their devices. Speculation built as to when Apple would follow suit. The iPhone 6 launch gave the public - or at least the tech community - what they wanted, with even more on top.

…The company is finally including the short-range wireless technology known as near field communications or NFC into its latest smartphone, the iPhone 6 and the bigger iPhone 6 Plus. It also announced a new digital wallet called Apple Pay, which can be accessed securely using its fingerprint Touch ID technology introduced in the iPhone 5S.

While there was excitement for the launch - for Apple Pay to function, retailers needed to have their payment infrastructure set up to accept NFC. Today, this is relatively standard, and most card payment devices feature NFC acceptance, but back in 2014, this wasn’t the case. At that time, much of the payment infrastructure in the United States still relied on swiping a card at the point of sale.

Getting Contactless Going

With the lack of NFC acceptance devices, one of Apple’s main competitors saw an opening. In early 2015 Samsung acquired and integrated LoopPay. LoopPay was a start up that enabled payments via a Samsung phone - even if the Point of Sale was still swipe only. The LoopPay functionality was embedded in the Samsung Pay wallet and became known as Magnetic Secure Transmission (MST).

MST was a USP for Samsung, at least for a while. When NFC became more widely available, MST lost its relevance. For most Android users Google Pay eventually became the goto application for mobile payments on the platform. (Google Pay was available across the whole Android ecosystem, whereas Samsung Pay was restricted just to Samsung devices.) Samsung cannot be blamed for trying though, and it’s hard to underestimate just how nascent the market for contactless payments was back in 2014. This from Visa:

Contactless payments, also known as Tap to Pay, arrived in the U.S. in 2014 with the launch of mobile wallets, however adoption remained nascent until 2018 when Visa financial institutions began issuing contactless cards in earnest.

On the other hand, in the UK, contactless payments were well established by 2014. There had been a big push in the run up to the 2012 Olympics for card acquirers, and large merchants, to add contactless payments. All London Olympics venues encouraged contactless payments, and over 2,000 devices were deployed, but as Visa was one of the main sponsors, only Visa cards could be used.

Other than the Olympics, the London transport network enabled contactless payments in 2012, initially on buses, with the Tube (Metro) following in 2014. From 2012, large retail chains were courted to add contactless payments. Initially, retailers needed separate devices just for NFC acceptance. Over time, the technology converged to a single device and got smaller. Today, contactless payments can be accepted on devices not much bigger than a payment card itself.

In a busy mega city like London, the introduction of contactless payments worked a treat. They’ve allowed for a much faster checkout experience than a Swipe, or a Chip and Pin transaction. They’ve made long queues move quicker, and soon most consumers wanted to pay with contactless.

One thing became clear. In every market where it launched, Apple Pay led to an acceleration in contactless payments. In the US - an iPhone centric market - the launch of Apple Pay led to more retailers deploying NFC technology in the years that followed. But the change was piecemeal, at least initially. In 2017, only 1% of Visa face-to-face transactions in the US were contactless. Yet by 2021, this had risen to 10%, and in 2023, this was now one in three. Apple Pay was a large driver of this. Most issuers only offered contactless following the demand created by the inclusion of NFC in iPhones. Having launched in 2014 users saw that it was fun to pay with Apple Pay, and retailers didn’t want to risk losing a sale if the cardholder couldn’t pay how they wanted to. Nothing changed overnight, but gradually, the market shifted.

One area where Apple Pay has undoubtedly accelerated innovation is with the Wallet app. Here Apple Pay has been a boon for fintechs. If you create a new account with a financial institution, then with Apple Pay, there’s no need to wait days for a credit or debit card to arrive at your home address. A card can be immediately loaded onto the wallet on an iPhone and then used with no delay - a great help when cards expire, are lost or stolen, or for a fintech to get a customer spending quickly.

For some users dropping the physical card entirely is a choice they are choosing to make. In a recent New York Times article, it was noted that many from Generation Z leave their wallets at home entirely these days. (Generation Z is defined by the Pew Research Centre as those born from 1997-2012.) This can be especially true as some US states allow users to store a driving license within the Apple Wallet app. A 19-year-old interviewed in the article, emphasising how she leaves her wallet at home, states “if a store doesn’t accept Tap to Pay, I won’t give them business”. Apple Pay has played a large part in making this possible.

Don’t Forget Biometrics

At the start of this post I asked the question: Why was Apple Pay such a big deal? And I answered because Apple Pay accelerated contactless payments.

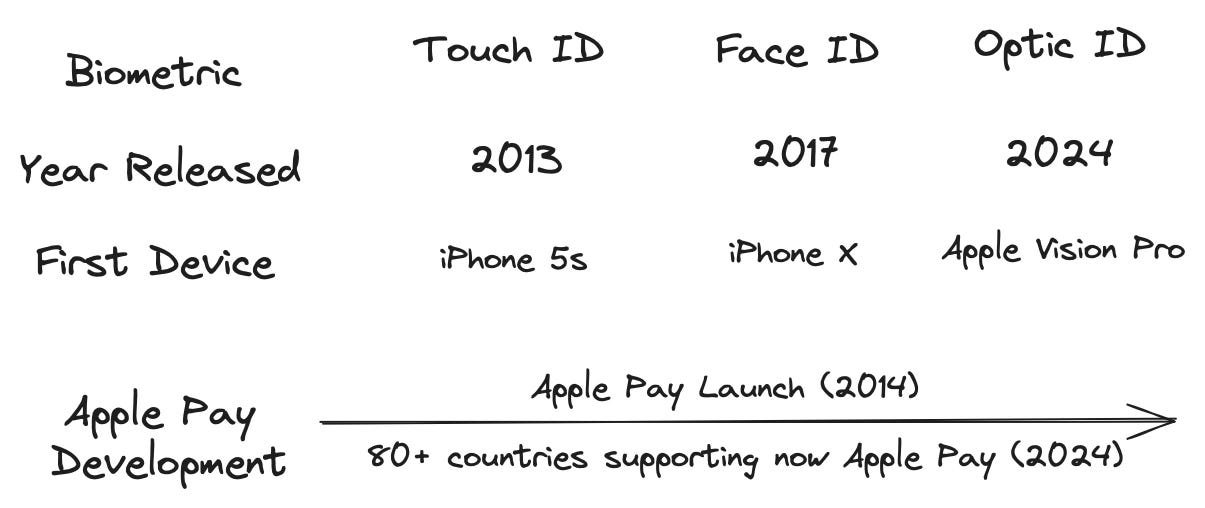

But there’s another side to this. Usually, contactless payments have a limit set above which additional authorisation is required - this limit is £100 in the UK. Apple Pay accelerated the use of on-device biometrics to make this process much easier. Quite simply, biometrics allows a physical feature, such as a thumbprint or a face scan, to be used to authorise a payment. So in a physical retail store, there’s no need to enter a PIN number - or to provide a signature - to complete a transaction. Instead, Touch ID on older iPhones and Face ID on newer ones takes on the role of authorising a transaction.

As a company that considers itself at the forefront of data security and privacy, without biometrics, Apple may never have launched Apple Pay. With Apple Pay, card numbers are never stored on the device, nor or Apple’s servers. Biometrics are safer and more secure than any other option for the benefit of both the consumer making the payment and the business selling their products.

Now with growing interest in Virtual Reality (VR), Augmented Reality (AR), and what Apple calls Spatial Computing, biometrics can evolve yet further. The Apple Vision Pro contains a technology called Optic ID.

In the same way that Touch ID revolutionized authentication using a fingerprint and Face ID revolutionized authentication using facial recognition, Optic ID revolutionizes authentication using iris recognition. Optic ID provides intuitive and secure authentication that uses the uniqueness of your iris, made possible by Apple Vision Pro’s high-performance eye-tracking system of LEDs and infrared cameras.

With a look, Optic ID securely unlocks your Apple Vision Pro. You can use it to authorize purchases from the App Store and Book Store, payments using Apple Pay, and more. Developers can also allow you to use Optic ID to sign into their apps. Apps that support Touch ID or Face ID automatically support Optic ID.

The reception to Optic ID has been muted so far, reflecting the fact that few Apple Vision Pro headsets have been sold, and that it’s still only available in the US. Yet Apple’s description makes it clear that Optic ID is going to be the most intuitive and secure way to authenticate payments with a headset. Emphasising the security angle, at WWDC23, when unveiling Optic ID, it was stated that even identical twins have a different Iris composition.

If only an iris scan is needed to buy a movie or a new app, working in this new way will also allow for seamless payments. There’s no doubt some users will be concerned about the privacy ramifications of this, much as they were when Touch ID and Face ID first came out. However, Apple will be on hand to explain why and how it’s very secure and ensures that users’ data is safe. Optic ID has provided another illustration of how Apple Pay has enabled secure payments across multiple form factors. You can now pay with a phone, watch, headset - what will be next?

Note: Contactless payments and Tap to Pay are the same thing. I may use them interchangeably at times. Also despite the different form factors, Apple Pay payments - whether on a Watch or Phone - are considered contactless payments.

The pandemic had more to do with the step change in NFC acceptance than Apple, Google, Visa, Mastercard, etc had to do with it.