Three key trends driving payments (2023 review)

Several long-term trends have accelerated this year and will continue into 2024

The Season For Predictions

It’s that time of the year when many organisations publish their 2023 reviews and their predictions for 2024. (For example, Visa’s is here.) These posts can be valuable, but such annual predictions often tend to reflect the current stage of a hype cycle. What’s hot at that moment. And what many firms have placed their bets on for the coming year.

In one year, not too much changes, but over a 5-10 year period, a lot can change. Often, the most impactful changes develop gradually over many years rather than burst onto the scene and have an immediate impact.

One example would be contactless payments, sometimes called tap to pay. The first big push with contactless payments in the UK was in the run-up to the 2012 Olympics in London. At that time, many businesses were sceptical of investing in the technology required to accept contactless payments. Yet in 2022, contactless payments comprised 27% of all payments in the UK. And this will continue to rise.

As an opposite example. Blockchain has often been mentioned as an emerging trend that can significantly impact payments. Views will be split on the exact effect that Blockchain has had so far. But it would be hard to argue the impact has been in line with the hype generated.

Yet, it can be helpful to look back at the prior year, especially in the context of long-term trends, as change is often incremental rather than exponential. When compounded over many years, large shifts can occur, which will have seemed inevitable.

Gloal Megatrends and Payment Trends

Even though it may seem obvious, it’s worth saying that payments and fintech do not exist in a vacuum. Technological progress is a reflection of broader society. With this in mind, looking at the bigger picture and understanding the key factors shaping the world over the long term can be helpful. PWC explains these so-called Megatrends in their report Five global shifts reshaping the world we live in as:

Deep and profound trends, global in scope and long-term in effect, touching everyone on the planet and shaping our world for many years to come.

The Megatrends themselves are Climate Change; Technological Disruption; Demographic Shifts; Fracturing World; and Social Instability. Often, these Megatrends overlap with each other. Key payments trends link to these global Megatrends. And global changes impact the payments technology businesses and consumers interact with daily.

These three key trends driving payments are not the only ones. There are others we could list. But in the context of long-term impact, impact in 2023, and broader context, these three below are worth exploring further.

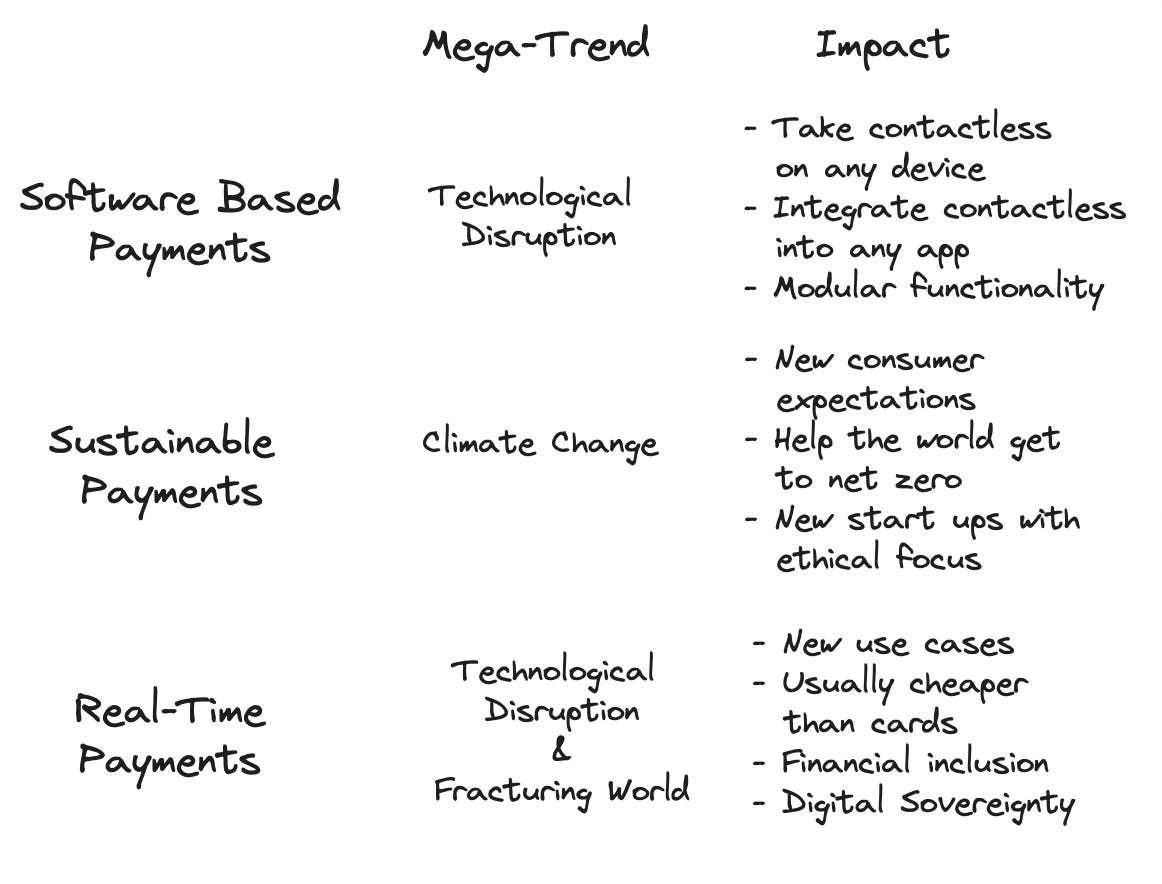

Payment Trend 1 - Software Based Payments

Discussed in more detail in the earlier post How Software Disrupts Payments, SoftPOS technology has matured this year. The ability to take payments from a standard Android device or an iPhone without any additional payment hardware is now becoming a familiar technology. It had been some years to get to this point, with various regulations evolving over the past few years. But 2023 was the time for SoftPOS to-go mass market.

From large payments companies such as Stripe and Adyen, to smaller players focused specifically in this area, such as Mypinpad, Yazara and Soft Space. There are a variety of SoftPOS solutions availible to meet customer needs. And with a fast onboarding process, a business can download an app and take payments directly from their handset within minutes.

In the UK the largest challenger banks, Revolut and Monzo, have launched SoftPOS this year. Combined, these banks have over 13m personal accounts and many business accounts. The ability to accept contactless payments can now sit alongside core banking functions within their mobile banking apps.

Whilst we are still early in the SoftPOS adoption curve, Revolut and Monzo have shown that by offering SoftPOS any bank can become a payments company. Doing so can enhance customer stickiness and generate new revenue streams. Offering contactless payment acceptance will become a standard part of a retail bank’s product offering in due course.

The prominence of software in payments is much wider than just SoftPOS. When an app sits on a consumer or merchant device, it can open up a wide variety of different services and use cases. New solutions can be added to the original app in a modular approach. Embedded Finance and Buy Now Pay Later (BNPL) are other examples that have also benefitted from this.

Key Megatrend: Technological Disruption. Take contactless payments anywhere on any device. Integrate contactless payments into any app. A modular approach to new functionality and solutions, so companies can widen reach across the payments value chain.

Payment Trend 2 - Sustainability in Payments

With the recent conclusion of the COP28 summit in Dubai, climate change has been top of the news agenda again - with all participants committing to:

take actions towards achieving, at a global scale, a tripling of renewable energy capacity and doubling energy efficiency improvements by 2030… accelerating efforts towards the phase-down of unabated coal power, phasing out inefficient fossil fuel subsidies, and other measures that drive the transition away from fossil fuels in energy systems, in a just, orderly and equitable manner, with developed countries continuing to take the lead.

The wordy final statement may reflect the compromise required to get this agreement over the line! These big summits may be great for capturing the news agenda for a few days, but the hard work of transitioning to net zero will go on every day.

Contactless payments can play a crucial role in scaling the adoption of electric vehicles (EVs). It's the most efficient way to pay for EV charging facilities. Organisations such as Siemens, may opt for contactless and QR-code options when rolling out EV charging. Having a wide range of payment options may speed up adoption across the network.

As detailed in How Payments Can Help Save The Planet, even in the US, 50% of new vehicle sales will be EVs by 2030. And despite some recent exemptions, by 2035, only zero-emissions vehicles will be permitted to be sold in the EU. With this in mind, payment technology will play a key role in accelerating this growth.

Additionally, plastic payment cards, whether credit or debit, have an environmental impact. For instance:

Creating one plastic payment card incurs the same carbon emissions as five plastic carrier bags. Something most of us have been cutting down on.

Several Scandinavian banks have started to provide cards made from recycled ocean plastic. This change can have a big impact, given that 70% of the payment card body can be made from recycled ocean plastic.

Plastic is also removed from the ocean as part of the process. Therefore, there is an environmental benefit from two angles.

Several fintech businesses focused on sustainability have emerged in 2023, and many more will follow in the decade ahead. kleen hub is focused on utilising re-useable packaging with their TAP&REUSE™ technology. Glad is building a carbon removal payment card. And Cogo is providing data solutions to help businesses, including banks and fintechs, provide climate impact data to their custome

Key Megatrend: Climate Change. Technology helping businesses to meet their net zero ambitions. Consumers see a focus on sustainability as a must have, not a nice to have.

Payment Trend 3 - Retail-Time Payments

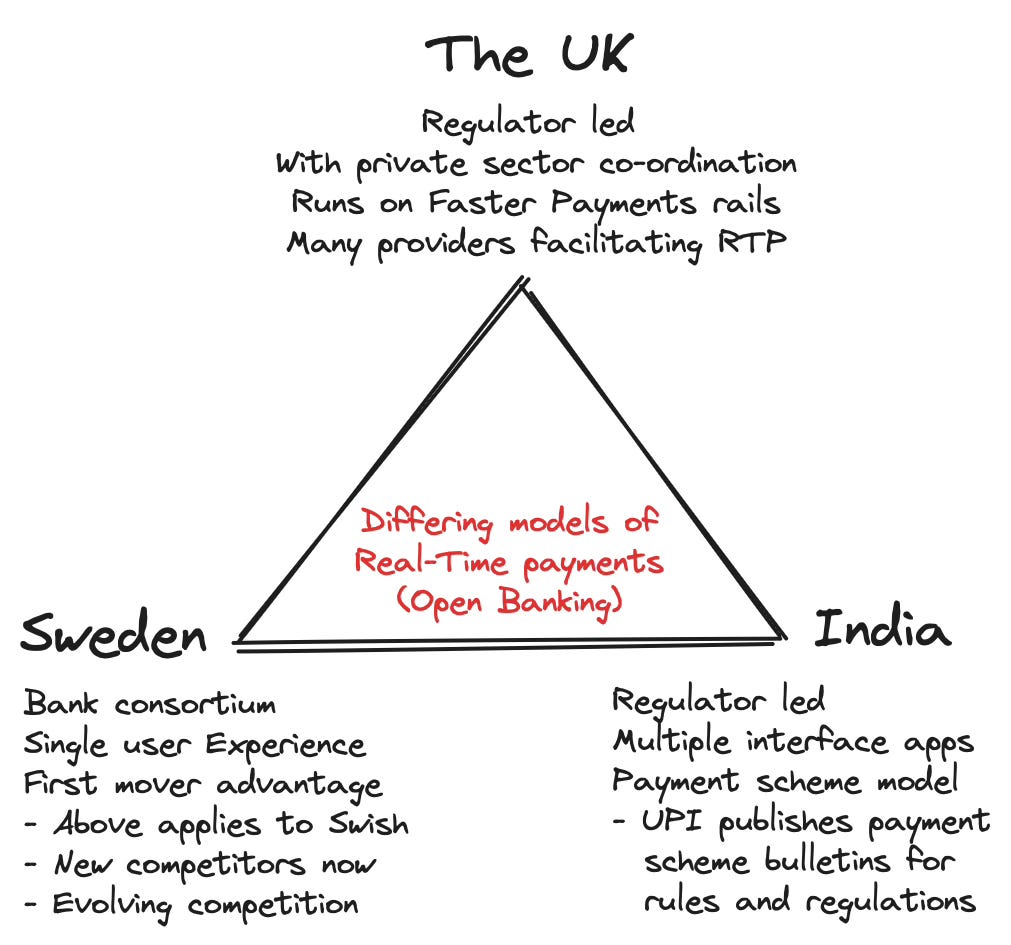

Retail-Time Payments (RTP), is sometimes known as Account-to-Account payments, and sometimes known as Open Banking payments. The ability to make a payment from one bank account directly to another with funds appearing in the other account within seconds. Payments can be sent outside of banking hours, such as on weekends or bank holidays, and still received instantly.

RTP takes on different forms in different countries. In a significant development, FedNow launched in the US in the summer of 2023. FedNow enables the possibility of retail time payment infrastructure for all banks. Many banks have signed up, with more financial institutions to be be added soon (the current list of FedNow participants is here). And non-bank organisations such as Plaid have integrated FedNow into their payment stack.

In the UK, hundreds of companies are authorised to provide Open Banking services, and the system operates on the faster payments rails. Around 12m transactions a month are made via Open Banking in the UK. Compared to Sweden, the UK is lagging behind when it comes to RTP. Swish was created by a consortium of banks in Sweden in 2012 and now sees more than 85m monthly transactions. Swish’s success has come from this strong local collaboration and a user-friendly app interface.

However, the biggest story regarding RTP is the growth of UPI (Unified Payments Interface), India’s RTP scheme. Since its inception in 2016, UPI has grown from a standing start to more than 11bn monthly transactions.

In 2022, India’s full-year RTP volumes reached 89.5bn, with 2023 bound to surpass this significantly. This growth of UPI has been a boon for financial inclusion. Many citizens are now making cashless payments for the first time through UPI. And various fintechs are working to build additional products and services on top of the core UPI offering.

Key Megatrends: Technological Disruption. Many use cases - both existing and new - can be built upon with RTP. Where use cases benefit all participants in the ecosystem, growth will be discernible and usually cheaper than card payments.

Another Megatrend can also apply to RTP: Fracturing World. More and more countries seek local first initiatives to sit alongside global card networks such as Visa and Mastercard. Digital sovereignty has become a key discussion point - can critical systems and infrastructure, including payments, function solely within a country’s own borders? And not be affected by outside forces. Many countries that have succeeded with RTP also have successful domestic card schemes (India, Brazil, China, etc).

What About Artificial Intelligence?

There’s no doubt that Artificial Intelligence (AI) has been the big story of the past 12 months across all industries and sectors. Blackstone has called AI the “Megatrend of Megatrends”, and in payments, like everything else, AI will be a part of everything.

As with the emergence and normalisation of the internet - at some point, we’ll stop thinking of AI as a technology in itself, and more as an enabler for everything. So I haven’t mentioned AI as a key trend driving payments at this time. But I'll look in a future post at the impact AI on the payments industry.

Thanks for reading Payments Culture!

Note that views expressed on this Substack are my own and do not represent any other organisation. Also nothing I say should be taken as investment advice.

Really appreciate your balanced view!

RTP = Real Time Payments vs Retail Time Payments