Incentivising Open Banking

Changing consumer behaviour isn’t easy

Shifting consumer behaviour requires a strong incentive.

In payments, this can start as a monetary incentive, but a better user experience and a strong network of acceptance are needed to embed any change.

Open Banking has had a big push.

There have been new market entrants, M&A from large payment firms (e.g. Visa buying Tink), and significant investment from venture capital.

Not too long ago, businesses with annualised revenue of less than $5m were achieving unicorn valuations. It was all about the future growth potential in Open Banking.

Yet, in Western economies, cards still rule over other payment methods, and the growth in Open Banking hasn’t materialised as expected. And with so much investment in this space, Open Banking is very competitive, leading to price pressure.

Or is the tide turning? Recently, an announcement was made, and shared widely that:

there are now 10 million consumers and small businesses regularly benefiting from using open banking technology

But what’s the definition of regularly?

Yes, there’s an average of more than 10 million Open Banking payment transactions per month in the UK, but card payments exceed 2 billion a month.

In January 2024, the ratio of card payments to Open Banking payments was 0.7%. This improved slightly to 0.8% in April - the most recent data available (Sources: UK Finance, Open Banking). This still means that for every Open Banking payment, there are 120+ card payments.

From a payments perspective, Open Banking still has a long way to go.

The focus has too often been on the benefits to businesses rather than consumers. But what can be done to incentivise consumers to use Open Banking? And what are the incentives for merchants to offer it? Here are some ideas.

1. Offer A Discount At Checkout

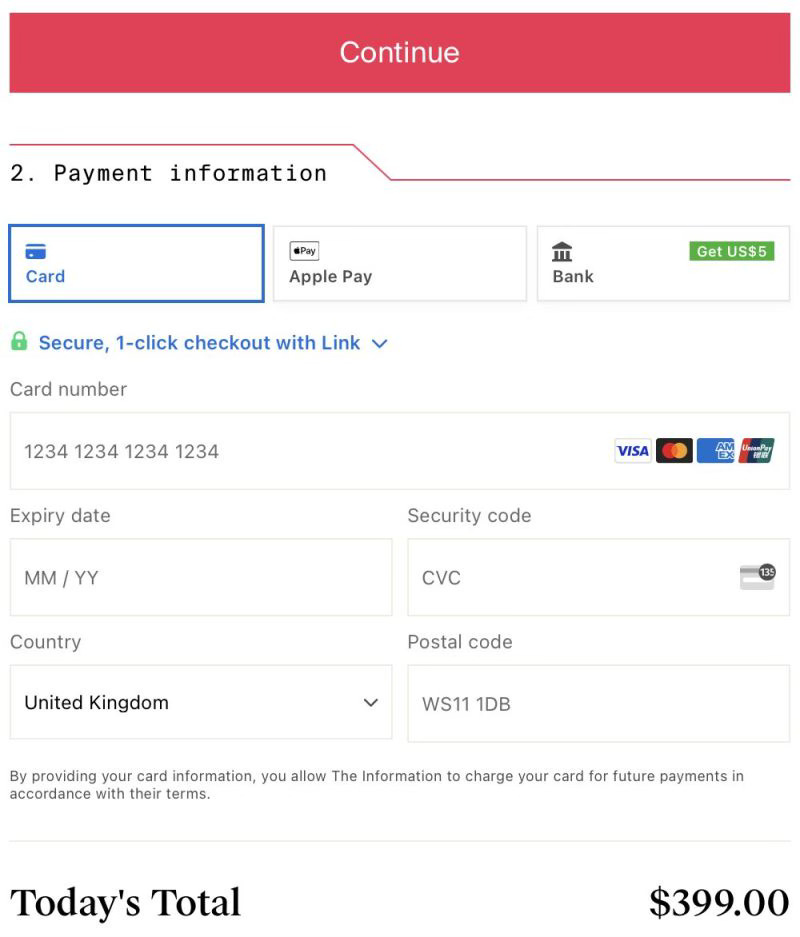

Below is the checkout page for the technology news website The Information.

This is an example of how businesses can incentivise consumers to pay with Open Banking (Pay By Bank). Customers can pay by card, or directly from their bank account. If they choose the latter they will pay $5 less than if paying by card.

How do the economics work?

Let’s assume the average fee to accept a card payment in the US is around 2.5%.

This means processing a $399 payment costs $10 (2.5% of $399).

With Pay By Bank, despite offering a discount of $5, the merchant is $5 better off.

The consumer is offered a discount of 1.25% of the total transaction value.

The Information saves 50% of the cost compared to processing a card payment.

(In reality, most businesses pay more than 2.5% for card payments, and there are fees for bank payments. However, the difference between the two options will be like the example above.)

On the downside, with Pay By Bank, the consumer:

Doesn’t get any rewards points or cashback from their card issuer, which is often worth more than the 1.25% discount.

And with a direct bank payment, there’s no ability to raise a chargeback.

In the above example the discount offered is very clear, but with card payments, the level of rewards or cashback can vary greatly depending on the type of card used.

A regulated debit card likely offers no rewards or cashback, and the merchant fees to accept it are low. A card such as the Chase Sapphire Reserve has a high acceptance cost but offers many perks and rewards for the cardholder.

Referring to the example from The Information, users opting for a basic debit card are likely best opting for the $5 discount. If they have a high-end credit card with a big annual fee, they’ll be better off using the card, and getting their issuer’s rewards.

The hope for businesses is that once a user has paid with a bank payment once, they will continue to do so. Thus bringing down their overall cost of accepting payments.

2. Offer A Discount For High-Value Transactions Only

In the UK and Europe, the largest fee component for card payments - interchange - is capped at 0.20% for debit cards and 0.30% for credit cards, at least for most transactions. With this much lower cost base for accepting card payments, generous discounts for Pay By Bank do not make sense.

Yet, offering a discount may still make sense for high value transactions - provided the discount level is lower than the card processing cost. If a business can offer a discount of 0.2% on a £5,000 transaction, then that’s a discount for the consumer of £10, but it would still be cheaper than the fee for processing a credit card payment.

Consumers are more likely to opt for Pay By Bank for a high value transaction.

Offering even a small discount may help steer users to Pay By Bank instead of a card payment, reducing costs for merchants, and also benefitting consumers (if they get a discount in the process).

3. Make It Easy

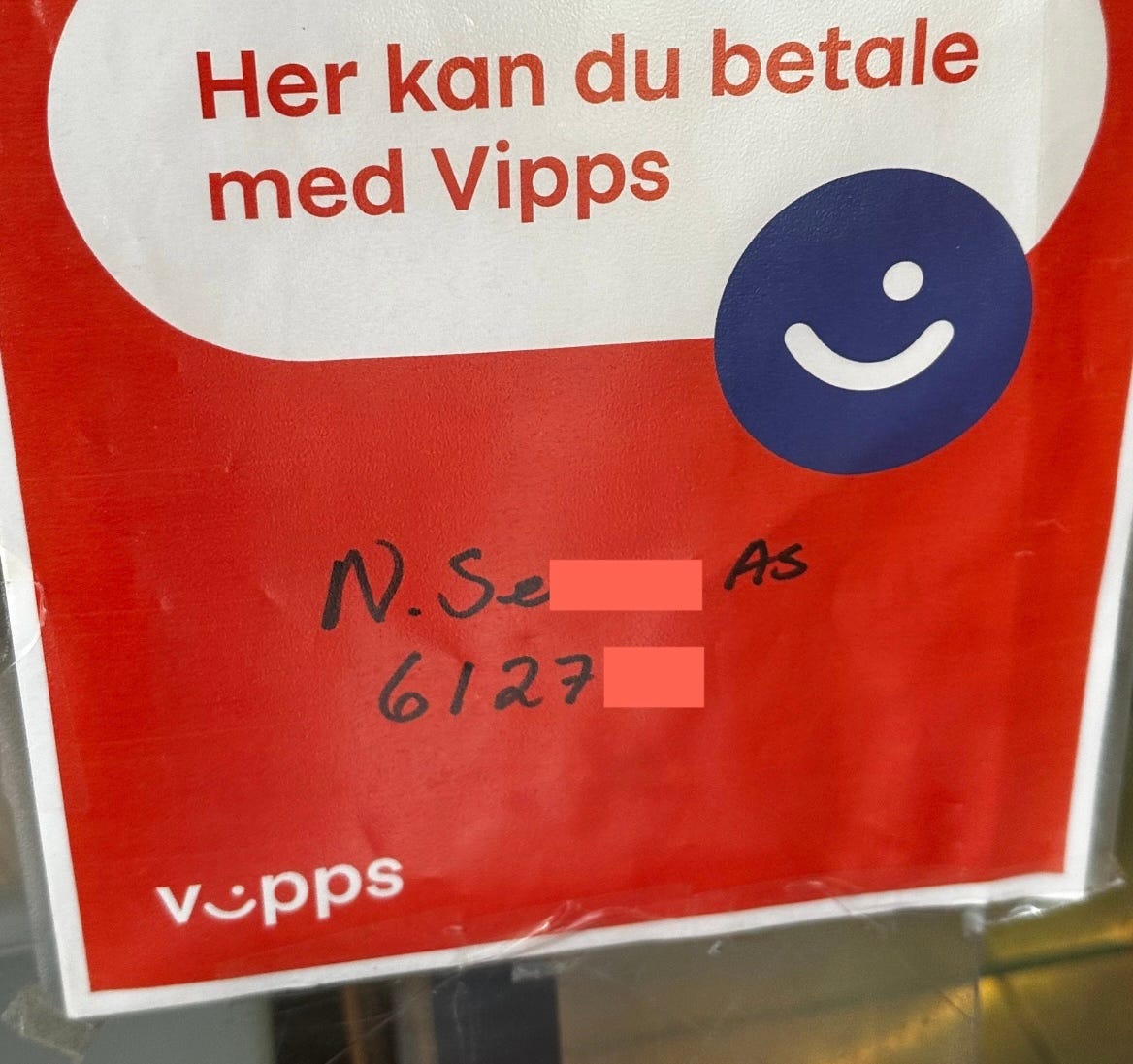

Sweden has Swish, and Norway has Vipps. Both are apps which enable bank-to-bank payments and can be used for person-to-person payments and payments to businesses.

Swish and Vipps make initiating a payment easy:

Scan a QR code at a business location.

Or scan a QR or on another user’s app.

Or enter the recipient’s phone number.

Or select the recipient from a user’s saved contacts.

The ease of use, instant settlement, and low cost mean that many businesses prefer Swish and Vipps over card payments. Yet they exist alongside card payments, rather than replacing them. For consumers, using these apps has become second nature.

As well as just payments, Swish and Vipps can be used to split a bill.

In the UK, there’s no equal to Swish or Vipps. Neobanks, like Monzo, are often used for bill splitting. Ten million adults have a Monzo account. While Monzo is popular, not everyone has an account. Swish and Vipps provide a bank-agnostic solution. As users get accustomed to these apps for bill splitting, they are more likely to use them for payments too.

Open Banking usually redirects to a mobile banking app to initiate a payment. However, with few exceptions, the world's most successful mobile wallet and account-to-account payment schemes are centred on an app agnostic of a user’s retail bank.

4. Incentivise Both Sides

Italy’s most popular non-card payment method is Satispay. Satispay is considered a mobile wallet topped up via a bank account - not Pay By Bank, as we commonly understand it.

For any payment method to be successful, there needs to be both supply and demand.

Demand from users seeking to use the payment method and a supply of merchants willing to offer it. Over time, this becomes a self-reinforcing cycle.

What we can learn from Satispay is the benefit of incentivising both sides.

From Software Synthesis:

Satispay’s closed loop model disintermediates the card schemes by banking merchants and consumers, in the mould of what PayPal and Block have achieved with Square and Cash App. This allows them to be extremely competitive on price, particularly for smaller purchases: free on transactions up to €10, and a flat €0.20 on transactions above this amount (offline).

This pricing model is competitive for merchants compared to card payments, especially for businesses with a low average transaction value. For a long time, in Italy, cash was king, and the local espresso bars were cash only. But with Satispay, many locations are now happy to accept cashless payments.

On the consumer side, prospective users were offered a €5 credit if they downloaded the Satispay app and made their first transaction. What is there to lose? If it works well, then why not use it again?

This growth model is only possible with a lot of money for marketing and incentive payments. It’s worked. Satispay has millions of users and hundreds of thousands of businesses. In reality this model is hard to replicate.

If you enjoyed this post, please consider liking this post or leaving a comment. It's much appreciated. Please consider subscribing to receive new posts via email or in the Substack app. If you’re an existing subscriber, you can upgrade your subscription to support this newsletter.

Further Reading (Payments Culture)

Other Interesting Reads 👀

Some articles - not necessarily payments and fintech related - that caught my eye:

Amazon Enlists TikTok, Pinterest in Quest to Sell Everywhere (The Information)

Chipmakers face a Labour crisis (Financial Times)

What Visa earnings really tell us (Popular Fintech)

Super informative!